The Housing Market Update September 2022 data from Columbus Realtors continued to support that the local housing shortage is as bad as ever, with low supplies and rising prices.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

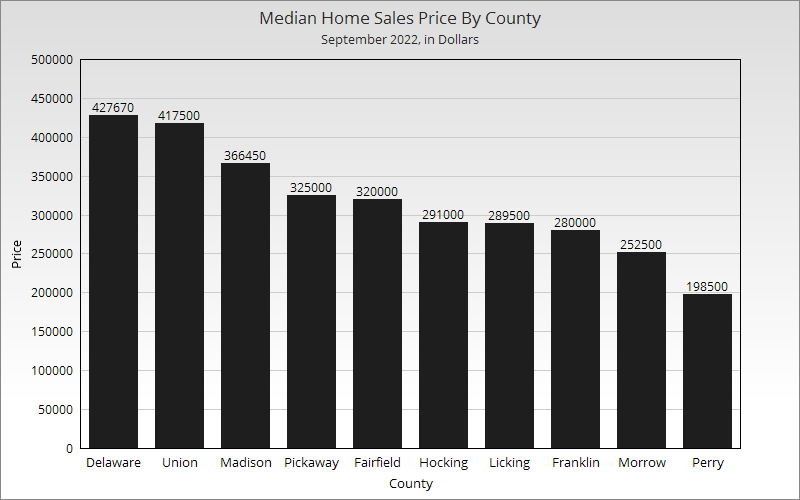

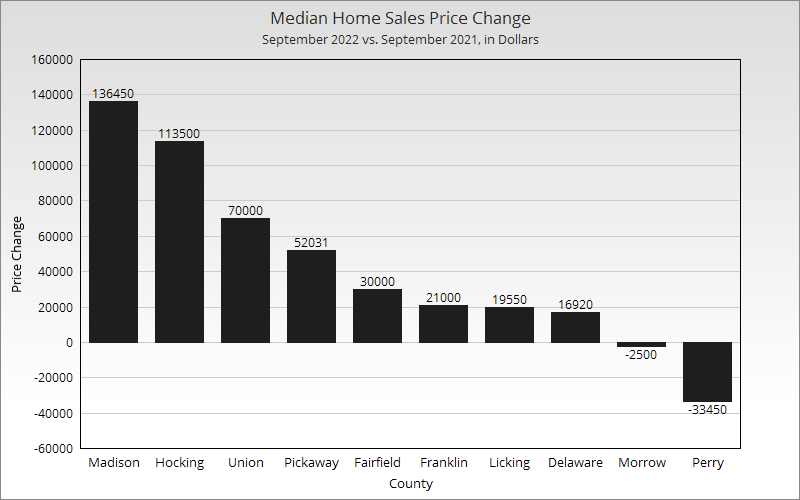

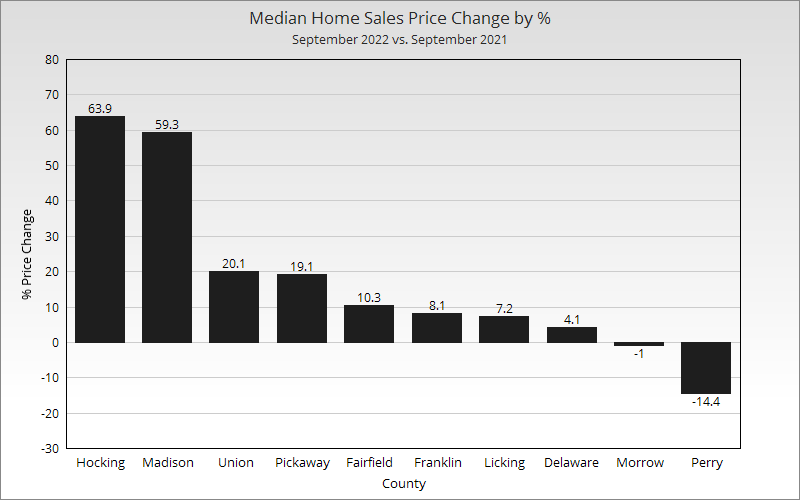

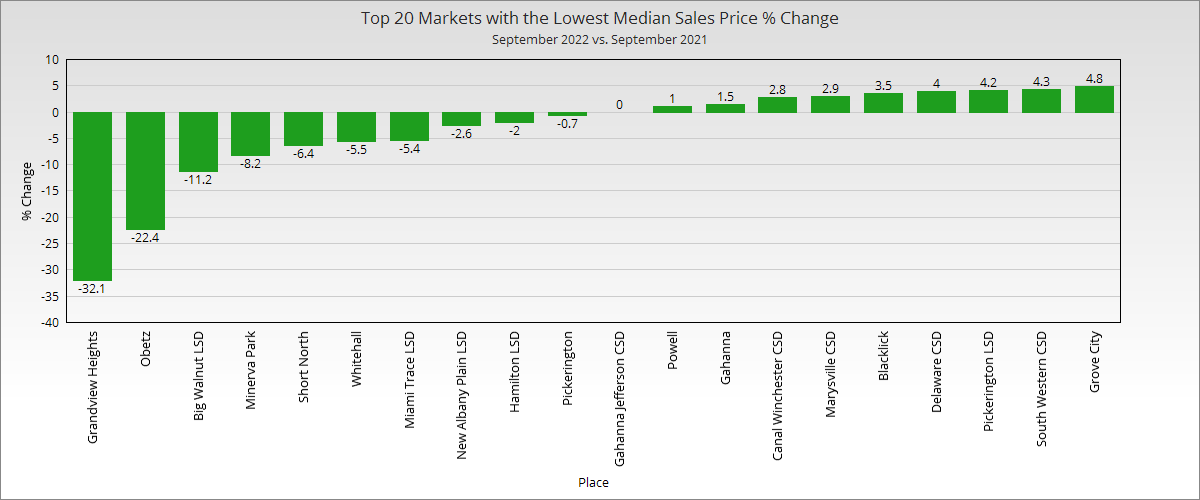

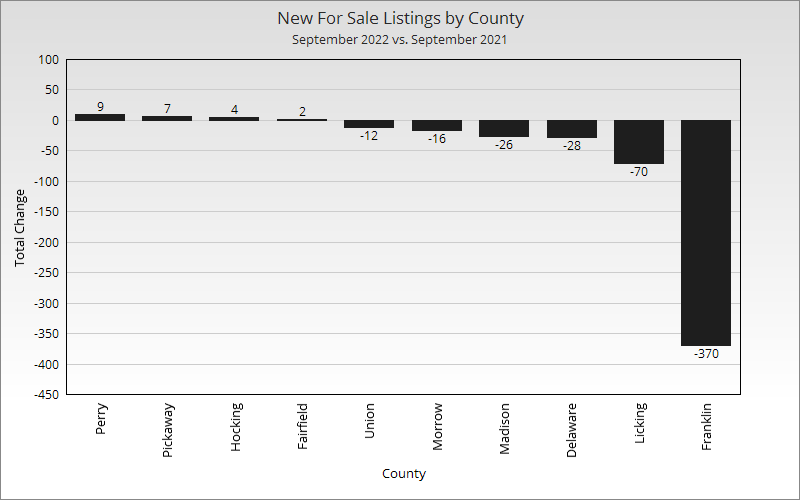

The least populated counties saw some of the largest swings either positively or negatively, which is typically the case given that prices can be determined by a much smaller number of home sales.

Overall Market Median Sales Price in September 2022: $316,812 Based on the 10 Columbus Metro Area counties, the metro price saw about a $10,000 increase over August 2022 and a more than $42,000 increase versus September 2021. Overall Market Median Sales Price % Change in September 2022 versus September 2021: +15.4%

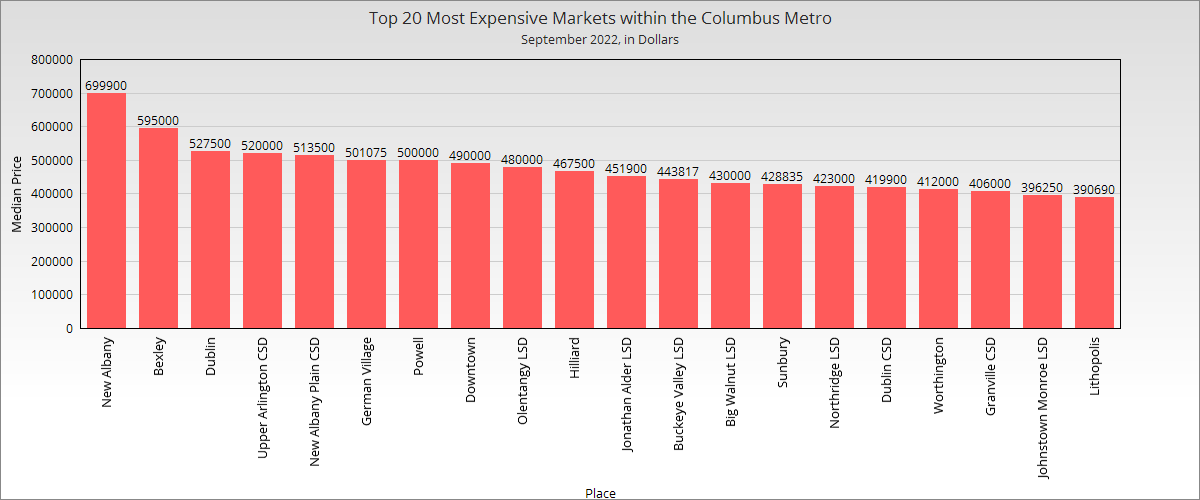

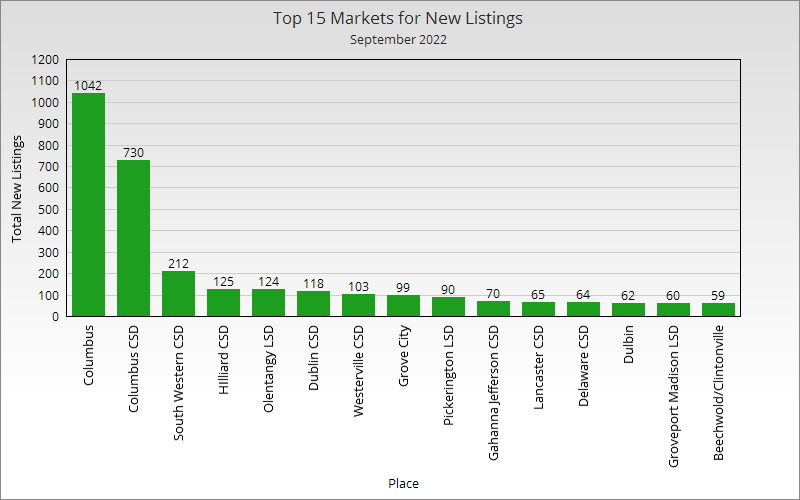

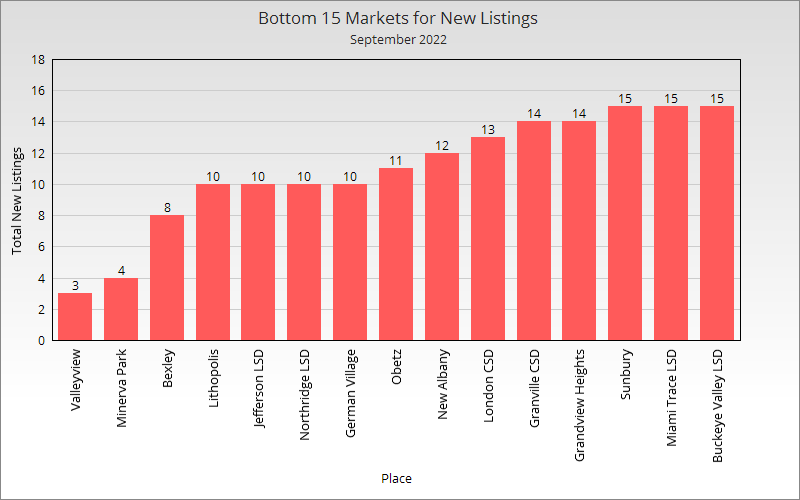

Now let’s take a look at individual neighborhoods and places within the metro area.

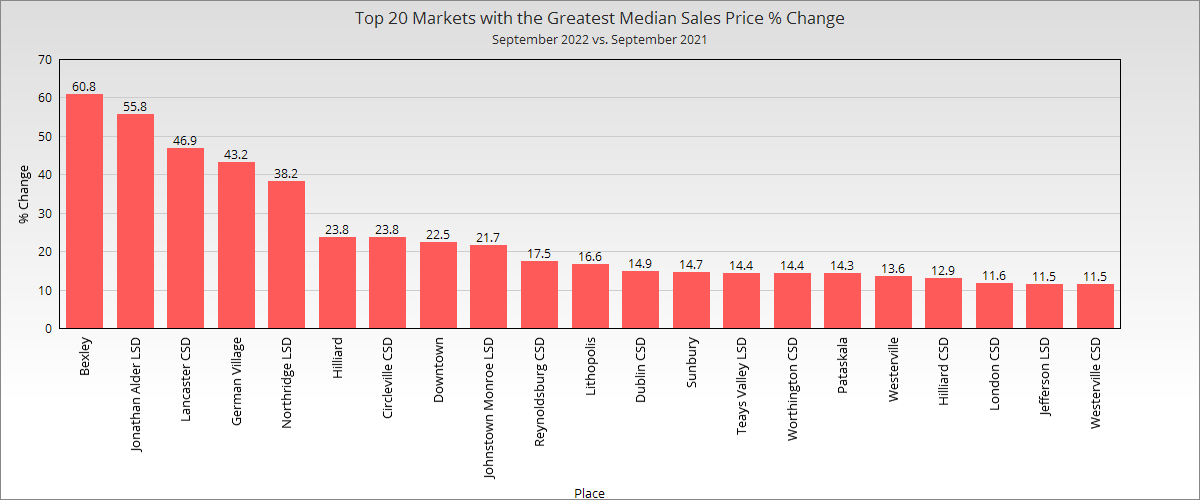

New Albany and some of the other expected suburbs continued to top the charts, but with prices not quite as high as over the summer.

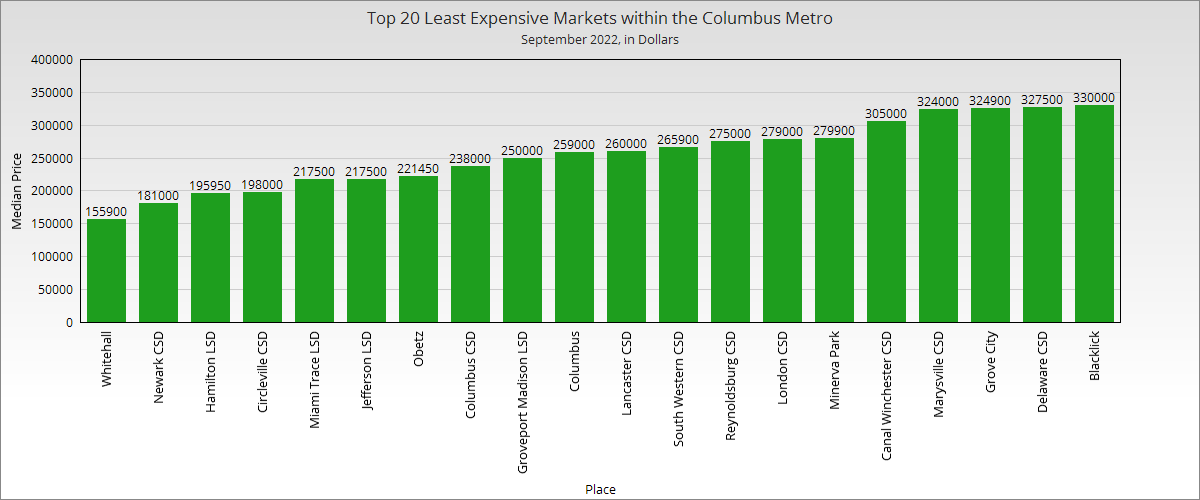

Just 4 local markets out of more than 50 remained below the $200K market in September. Columbus itself was in it usual spot closer to the *relatively* more affordable bottom.

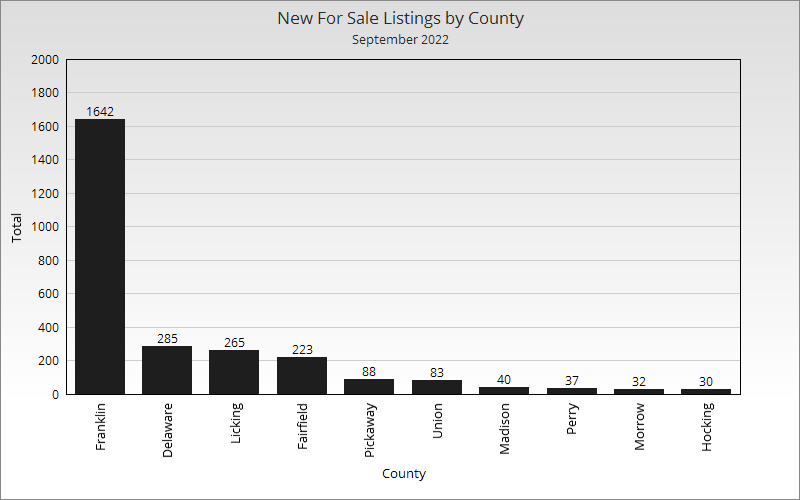

Total Metro New Listings in September 2022: 2,725 Total Metro New Listings Change from September 2021 to September 2022: -500 Year-over-year, new listings were down significantly across the metro area, but especially in Franklin County.

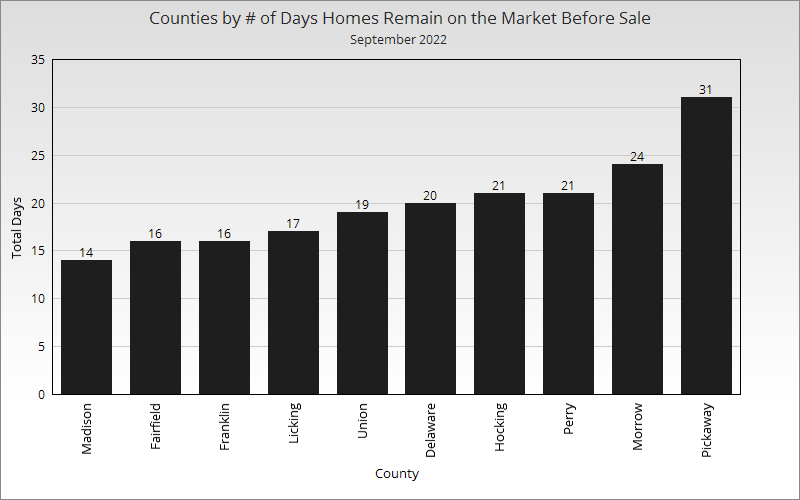

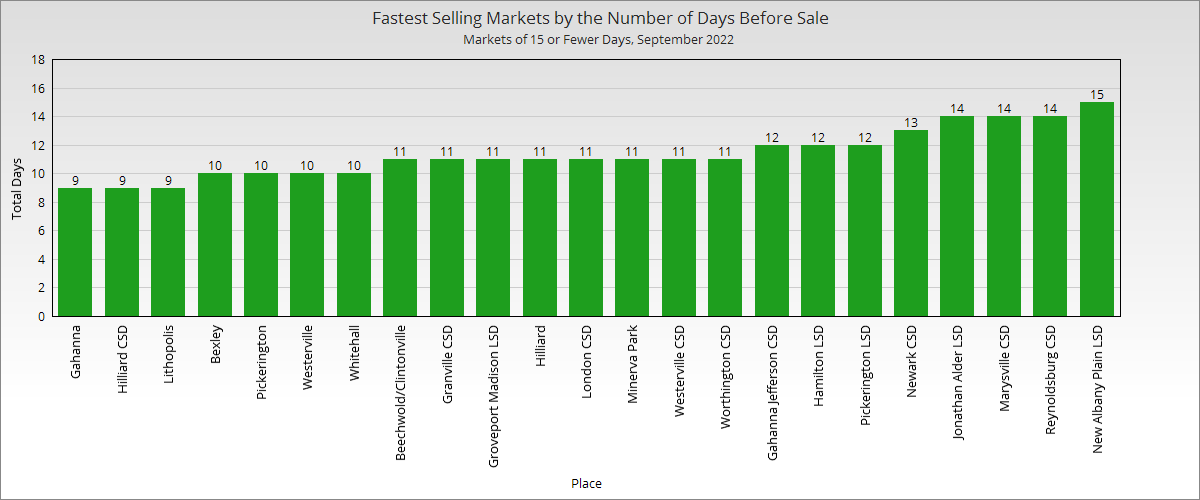

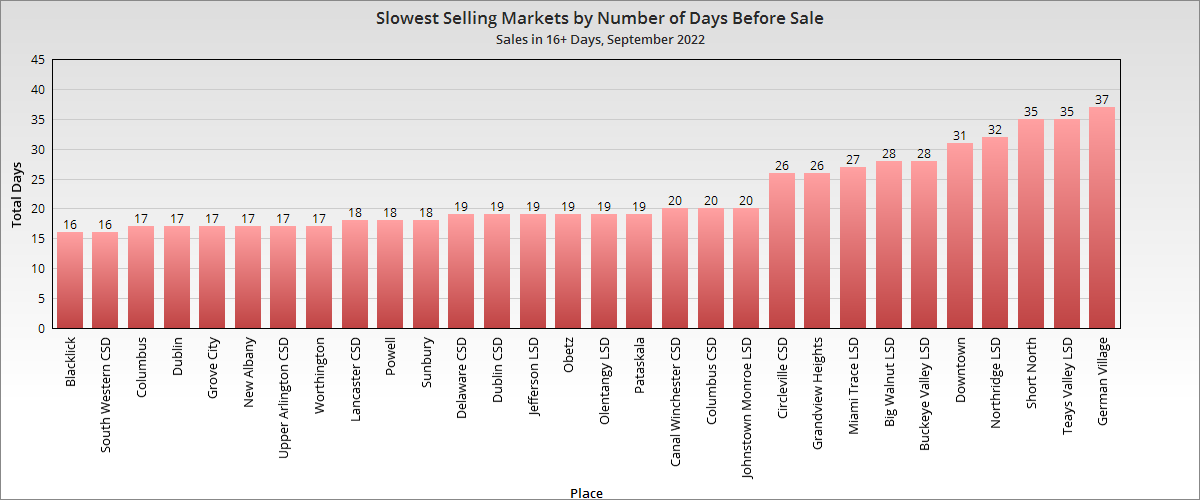

Average # of Days Homes Remain on the Market Before Sale for the Metro Overall in September 2022: 19.9 # of Days Homes Remain on the Market Before Sale for the Metro September 2021 vs. September 2022: -0.3 Homes across the market sold slightly faster than a year ago, but largely due to significant drops in a few rural counties. Most counties saw small increases.

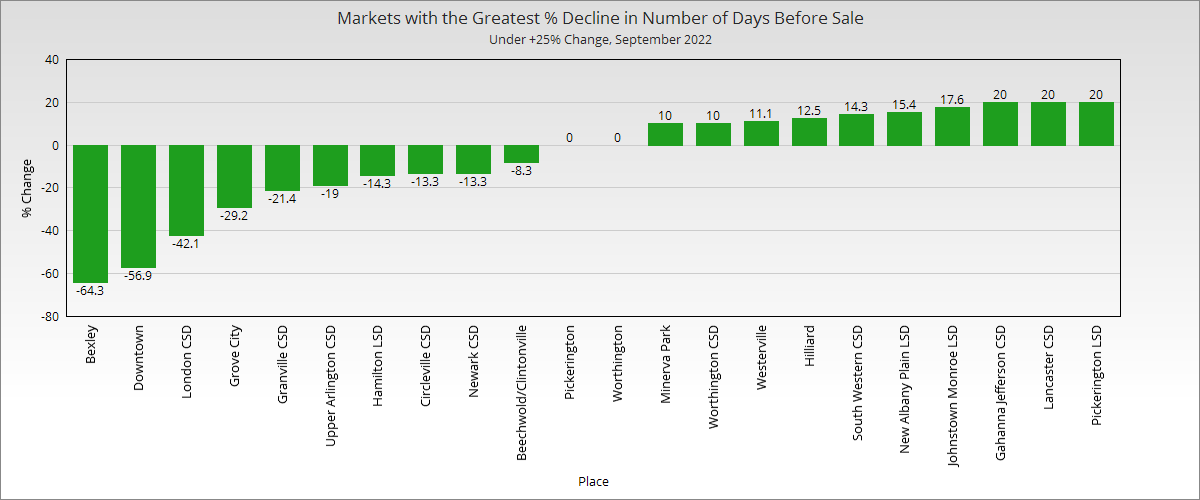

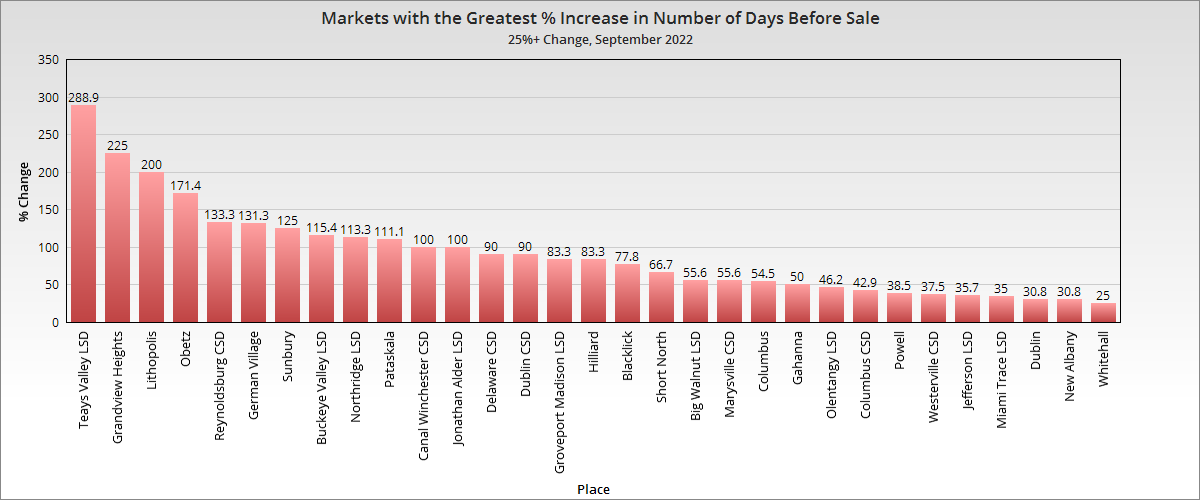

The vast majority of local markets saw substantial increases in the number of days before sale, which is pretty much the only measurement indicating the seller’s market may finally be showing some signs of weakness.

November home sales were down in Central Ohio for the 2nd straight month according to the Housing Market Update November 2013 data from Columbus Realtors. One main reason seems to be the culprit: There just aren’t enough houses to go around. Hot urban markets simply have a limited stock of homes with very few going up for sale at any one time, and builders still have not been building very much since the recession. Combined, the total number of homes for sale has declined to levels not seen since the early 2000s. This explains why most markets are still seeing gains in home prices while overall sales have fallen from the year before.

The bottom line is that demand is outpacing supply, and that situation doesn’t look to change anytime soon, especially in the urban core.

Here are the stats for the 21 major areas of Franklin County that I look at housing stats for.

Average # of Days Before Sale, November 2013 Urban: 57.4 Suburban: 89.4 Urban without Columbus: 56.3

Average # of Days Before Sale YTD Urban: 60.6 Suburban: 62.7 Urban without Columbus: 60.2

Top 10 Lowest Market Housing Supplies (Based on # of Months to Sell all Listings) 1. Worthington: 1.6 2. Upper Arlington: 2.1 3. Hilliard: 2.2 4. Minerva Park: 2.2 5. Bexley: 2.3 6. Clintonville: 2.4 7. Westerville: 2.4 8. Gahanna: 2.6 9. German Village: 2.6 10. Grandview Heights: 2.6

A healthy housing supply is considered to be around 5 months. Anything less than 3 months is considered very low. All of the 21 areas I looked at were below 5 months, indicating a county-wide shortage.

Average # of Months to Sell All Listings, November 2013 Urban: 2.8 Suburban: 3.6 Urban without Columbus: 2.7

Average % Change of Single-Family Home Sales November 2013 vs. November 2012 Urban: -1.7% Suburban: -12.6% Urban without Columbus: -0.5%

Average % Change of Single-Family Home Sales YTD vs. YTD 2012 Urban: +9.3% Suburban: +19.4% Urban without Columbus: +8.2%

Average % Change of Condo Sales November 2013 vs. November 2012 Urban: +23.3% Suburban: +52.8% Urban without Columbus: +26.6%

Average % Change of Condo Sales YTD vs. YTD 2012 Urban: +27.6% Suburban: +26.4% Urban without Columbus: +28.3%