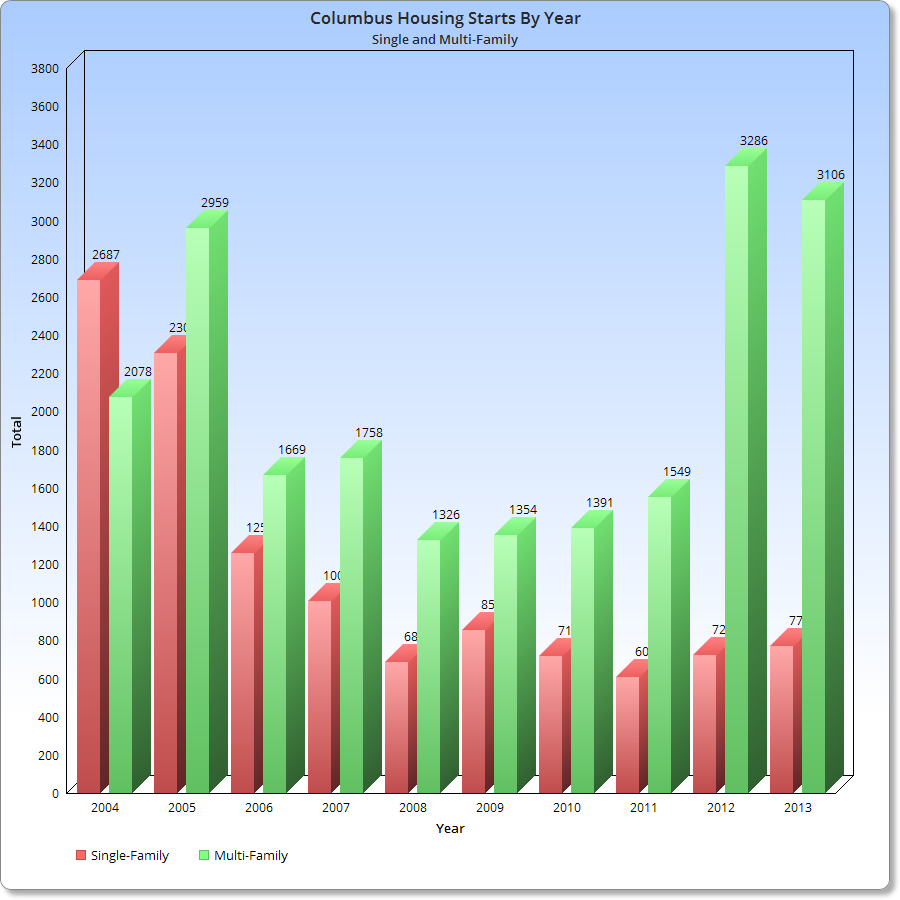

We’ve been hearing a lot the last few years about how residential construction has largely turned toward the rental variety, and no more so than in the urban areas. I have tried to document the level of activity in the city in my development page, but it doesn’t quite show what’s going on in the city overall. I did a little research and found some surprising realities that fully support the rental boom. The residential construction trends of Columbus have changed significantly in recent years.

Here is a graph of annual housing construction permits from 2004-2013 broken down by multi-family and single-family types. The chart above is based on the # of units, not the number of overall projects.

So what do the numbers say? Well, it raises some interesting questions. First, was the amount of single-family home construction on the decline before 2004 given the downward trend from that year through 2005? And was multi-family construction on the rise during the same period? Did the recession merely interrupt a trend that began more than a decade ago and resurfaced strongly in recent years? It’s hard to say for sure as I don’t have information before 2004, but regardless, it is clear that multi-family construction is the preferred residential preference right now by builders. Single-family home construction, however, has remained steady and well below its previous peak of the last decade.

This continued low level of single-family construction has likely contributed to the fact that area sales in that market have been down for several months now due to a lack of inventory. Prices, however, have risen.

December ended a 2-month decline in home sales for the area, with overall sales up 2.5% according to the Housing Market Update December 2013 data from Columbus Realtors.

Here are the stats for the 21 major areas of Franklin County that I look at housing stats for.

Top 10 December 2013 Sales Increases over December 2012 1. Minerva Park: +200.0% 2. Obetz: +200.0% 3. Reynoldsburg: +72.7% 4. Clintonville: +55.6% 5. Gahanna: +55.0% 6. Pataskala: +27.3% 7. Dublin: +15.4% 8. German Village: +10.0% 9. Worthington: +6.3% 10. Columbus: +3.8%

Top 10 Year-to-Date Sales Through December 2013 1. Columbus: 10,267 2. Dublin: 797 3. Upper Arlington: 719 4. Clintonville: 701 5. Westerville: 630 6. Grove City: 609 7. Hilliard: 556 8. Gahanna: 526 9. Reynoldsburg: 505 10. Pickerington: 312

Top 10 Year-to-Date Increases Through December 2013 Over 2012 1. Minerva Park: +51.9% 2. Gahanna: +31.8% 3. Pataskala: +31.0% 4. Reynoldsburg: +30.8% 5. Whitehall: +27.3% 6. Clintonville: +26.3% 7. Hilliard: +23.6% 8. Whitehall: +23.4% 9. Westerville: +21.9% 10. Bexley: +21.5%

Average Sales December 2013 Urban: 74.5 Suburban: 28.2 Urban without Columbus: 14.7

Average % Change December 2013 vs. December 2012 Urban: +40.5% Suburban: +6.4% Urban without Columbus: +44.2%

Average YTD Sales Through December 2013 Urban: 1,177.1 Suburban: 466.5 Urban without Columbus: 268.1

Average YTD % Change YTD Through December 2013 Urban: +15.7% Suburban: +19.4% Urban without Columbus: +15.3%

Top 10 Average Sales Price December 2013 1. New Albany: $563,187 2. Upper Arlington: $377,943 3. Bexley: $376,592 4. Dublin: $351,279 5. Downtown: $314,583 6. German Village: $303,136 7. German Village: $271,656 8. Hilliard: $249,811 9. Worthington: $232,741 10. Clintonville: $223,250

Top 10 Average Sales Price % Change December 2013 Over December 2012 1. Whitehall: +37.3% 2. New Albany: +32.8% 3. Pataskala: +29.6% 4. Reynoldsburg: +26.3% 5. Upper Arlington: +25.8% 6. Clintonville: +25.3% 7. Bexley: +23.7% 8. Hilliard: +21.9% 9. Gahanna: +19.6% 10. Dublin: +13.1%

Top 10 Average Sales Prices YTD Through December 2013 1. New Albany: $542,634 2. Upper Arlington: $365,143 3. Bexley: $352,214 4. Dublin: $336,048 5. German Village: $298,199 6. Downtown: $287,976 7. Worthington: $248,857 8. Grandview Heights: $223,185 9. Hilliard: $217,078 10. Gahanna: $199,546

Top 10 Average YTD Sales Price % Change Through December 2013 vs. 2012 1. Whitehall: +18.9% 2. Downtown: +14.0% 3. Minerva Park: +14.0% 4. Upper Arlington: +13.8% 5. Gahanna: +12.1% 6. New Albany: +9.8% 7. Reynoldsburg: +9.6% 8. Obetz: +9.0% 9. Worthington: +7.5% 10. Bexley: +5.8%

Average Sales Price December 2013 Urban: $218,764 Suburban: $233,048 Urban without Columbus: $227,832

Average Sales Price Change December 2012 vs. December 2012 Urban: -1.6% Suburban: +15.5% Urban without Columbus: -2.9%

Average Sales Price YTD Urban: $217,056 Suburban: $224,060 Urban without Columbus: $226,017

Average Sales Price % Change YTD Urban: +5.6% Suburban: +5.6% Urban without Columbus: +5.7%

Top 10 Fastest Selling Markets December 2013 (Based on Average # of Days for Listings to Sell) 1. Bexley: 26 2. Obetz: 42 3. New Albany: 47 4. Hilliard: 50 5. Clintonville: 51 6. Pataskala: 57 7. Gahanna: 58 8. Upper Arlington: 58 9. Reynoldsburg: 61 10. Grove City: 63

Average # of Days Before Sale, December 2013 Urban: 73.4 Suburban: 63.9 Urban without Columbus: 73.8

Average # of Days Before Sale YTD Urban: 61.3 Suburban: 62.9 Urban without Columbus: 60.9

Top 10 Lowest Market Housing Supplies (Based on # of Months to Sell all Listings) 1. Worthington: 1.2 2. Bexley: 1.8 3. Clintonville: 1.9 4. Hilliard: 1.9 5. Upper Arlington: 1.9 6. Grandview Heights: 2.1 7. Westerville: 2.1 8. Gahanna: 2.2 9. Minerva Park: 2.2 10. German Village: 2.3

A healthy housing supply is considered to be around 5 months. Anything less than 3 months is considered very low. All of the 21 areas I looked at were below 5 months, indicating a county-wide shortage. This shortage has only deepened over the last year, with December having the lowest number of available homes in nearly 15 years.

Average # of Months to Sell All Listings, December 2013 Urban: 2.7 Suburban: 3.2 Urban without Columbus: 2.6

Average % Change of Single-Family Home Sales December 2013 vs. December 2012 Urban: +28.5% Suburban: +14.3% Urban without Columbus: +30.8%

Average % Change of Single-Family Home Sales YTD vs. YTD 2012 Urban: +9.8% Suburban: +19.0% Urban without Columbus: +8.8%

Average % Change of Condo Sales December 2013 vs. December 2012 Urban: +20.5% Suburban: -4.2% Urban without Columbus: +20.5%

Average % Change of Condo Sales YTD vs. YTD 2012 Urban: +29.0% Suburban: +23.5% Urban without Columbus: +29.9%

November home sales were down in Central Ohio for the 2nd straight month according to the Housing Market Update November 2013 data from Columbus Realtors. One main reason seems to be the culprit: There just aren’t enough houses to go around. Hot urban markets simply have a limited stock of homes with very few going up for sale at any one time, and builders still have not been building very much since the recession. Combined, the total number of homes for sale has declined to levels not seen since the early 2000s. This explains why most markets are still seeing gains in home prices while overall sales have fallen from the year before.

The bottom line is that demand is outpacing supply, and that situation doesn’t look to change anytime soon, especially in the urban core.

Here are the stats for the 21 major areas of Franklin County that I look at housing stats for.

Average # of Days Before Sale, November 2013 Urban: 57.4 Suburban: 89.4 Urban without Columbus: 56.3

Average # of Days Before Sale YTD Urban: 60.6 Suburban: 62.7 Urban without Columbus: 60.2

Top 10 Lowest Market Housing Supplies (Based on # of Months to Sell all Listings) 1. Worthington: 1.6 2. Upper Arlington: 2.1 3. Hilliard: 2.2 4. Minerva Park: 2.2 5. Bexley: 2.3 6. Clintonville: 2.4 7. Westerville: 2.4 8. Gahanna: 2.6 9. German Village: 2.6 10. Grandview Heights: 2.6

A healthy housing supply is considered to be around 5 months. Anything less than 3 months is considered very low. All of the 21 areas I looked at were below 5 months, indicating a county-wide shortage.

Average # of Months to Sell All Listings, November 2013 Urban: 2.8 Suburban: 3.6 Urban without Columbus: 2.7

Average % Change of Single-Family Home Sales November 2013 vs. November 2012 Urban: -1.7% Suburban: -12.6% Urban without Columbus: -0.5%

Average % Change of Single-Family Home Sales YTD vs. YTD 2012 Urban: +9.3% Suburban: +19.4% Urban without Columbus: +8.2%

Average % Change of Condo Sales November 2013 vs. November 2012 Urban: +23.3% Suburban: +52.8% Urban without Columbus: +26.6%

Average % Change of Condo Sales YTD vs. YTD 2012 Urban: +27.6% Suburban: +26.4% Urban without Columbus: +28.3%

The latest numbers for the Columbus housing market from Columbus Realtors.

LSD=Local school district CSD=City school district

Top 15 Most Expensive Locations by Median Sales Price in October 2013 1. New Albany: $445,900 2. Upper Arlington CSD: $358,000 3. Downtown: $330,000 4. Powell: $305,000 5. Dublin: $302,125 6. Jefferson LSD: $292,500 7. Olentangy LSD: $288,500 8. Granville CSD: $272,000 9. New Albany Plain LSD: $262,500 10. Worthington: $249,900 11. Buckeye Valley LSD: $246,250 12. Big Walnut LSD: $238,500 13. Beechwold/Clintonville: $230,000 14. Bexley: $225,875 15. German Village: $217,500

Top 15 Least Expensive Locations by Median Sales Price in October 2013 1. Whitehall: $42,500 2. Lancaster CSD: $75,250 3. Hamilton LSD: $83,450 4. Columbus CSD: $84,200 5. Newark CSD: $87,450 6. Groveport Madison LSD: $90,150 7. London CSD: $94,500 8. South-Western CSD: $95,000 9. Columbus: $104,500 10. Circleville CSD: $110,250 11. Blacklick: $134,251 12. Obetz: $134,950 13. Canal Winchester CSD: $135,000 14. Grove City: $135,000 15. Reynoldsburg CSD: $136,200

Overall Metro Median Sales Price in October 2013: $149,302 Median Sales Price Change October 2012-October 2013: -$3,183

Top 15 Locations with the Highest Median Sales Price % Growth Between October 2012-October 2013 1. Hamilton LSD: +85.4% 2. Jefferson LSD: +69.8% 3. Downtown: +63.8% 4. Reynoldsburg CSD: +54.4% 5. Obetz: +51.8% 6. Jonathan Alder LSD: +50.4% 7. Sunbury: +36.5% 8. Beechwold/Clintonville: +28.6% 9. Westerville CSD: +20.2% 10. Minerva Park: +19.4% 11. Marysville CSD: +19.4% 12. Lithopolis: +19.0% 13. Northridge LSD: +17.4% 14. Circleville CSD: +16.7% 15. Granville CSD: +15.6%

Top 15 Locations with the Lowest Median Sales Price % Growth Between October 2012-October 2013 1. German Village: -16.3% 2. Lancaster CSD: -16.3% 4. Buckeye Valley LSD: -14.9% 5. New Albany Plain LSD: -14.6% 6. Canal Winchester CSD: -14.6% 7. Grandview Heights: -14.2% 8. Hilliard: -12.8% 9. South-Western CSD: -11.4% 10. London CSD: -11.3% 11. Dublin CSD: -10.8% 12. Dublin: -10.3% 13. Whitehall: -7.6% 14. Gahanna Jefferson CSD: -5.6% 15. Johnstown Monroe LSD: -3.7%

Overall Metro Median Price % Change October 2012-October 2013: -2.1%

Top 10 Locations with the Most New Listings in October 2013 1. Columbus: 1,107 2. Columbus CSD: 691 3. Westerville CSD: 177 4. South-Western CSD: 169 5. Hilliard CSD: 158 6. Olentangy LSD: 157 7. Dublin CSD: 123 8. Groveport Madison LSD: 91 9. Worthington CSD: 79 10. Dublin: 73

Top 10 Locations with the Fewest New Listings in October 2013 1. Valleyview: 0 2. Lithopolis: 0 3. Minerva Park: 2 4. Jefferson LSD: 5 5. Obetz: 5 6. Sunbury: 5 7. Northridge LSD: 9 8. Jonathan Alder LSD: 9 9. German Village: 9 10. Grandview Heights: 10

Overall Metro New Listings in October 2013: 2,693 New Listings % Change October 2012-October 2013: +5.9%

Top 10 Fastest-Selling Locations by # of Days Homes Remain on the Market Before Sale in October 2013 1. Johnstown Monroe LSD: 30 2. Powell: 31 3. Buckeye Valley LSD: 32 4. Grandview Heights: 39 5. Minerva Park: 42 6. Beechwold/Clintonville: 45 7. Northridge LSD: 45 8. Olentangy LSD: 46 9. Westerville: 46 10. Jonathan Alder LSD: 47

Top 10 Slowest-Selling Locations by # of Days Homes Remain on the Market Before Sale in March 2013 1. Circleville CSD: 118 2. London CSD: 107 3. Lancaster CSD: 106 4. Obetz: 105 5. Hamilton LSD: 96 6. New Albany CSD: 91 7. Granville CSD: 84 8. Jefferson LSD: 82 9. Big Walnut LSD: 81 10. Hilliard: 78 11. Reynoldsburg: CSD: 78

Overall Metro Average # of Days on Market Before Sale: 74.7

Top 10 Locations with the Best Change in # of Days on the Market Before Sale October 2012-October 2013 1. Lithopolis: +522.2% 2. Minerva Park: -77.25 3. Johnstown Monroe LSD: -74.6% 4. Buckeye Valley LSD: -71.7% 5. Jonathan Alder LSD: -69.1% 6. Grandview Heights: -64.2% 7. Powell: -62.7% 8. German Village: -61.2% 9. Northridge LSD: -54.5% 10. Pickerington LSD: -47.0%

Top 10 Locations with the Worst Change in the # of Days on the Market Before Sale October 2012-October 2013 1. Hamilton LSD: +190.9% 2. Obetz: +150.0% 3. Lancaster CSD: +86.0% 4. Sunbury: +50.0% 5. Circleville CSD: +45.7% 6. London CSD: +27.4% 7. New Albany: +14.6% 8. Worthington: +13.7% 9. Granville CSD: +9.1% 10. New Albany CSD: +8.3%

Overall Metro # of Days on Market Before Sale % Change October 2012-October 2013: -24.9%

The Columbus housing market August 2013 data from Columbus Realtors shows that the area continued hot, with record August sales and potentially a record year still in the making. For the region, sales were up 11% for August and are were up almost 23% for the first 8 months of the year.

I looked at the 21 major areas of Franklin County (11 urban, 10 suburban). Here is what the August market looked like.