A lot of requests for zip code data come into this site, so I thought it might be a good idea to provide some.

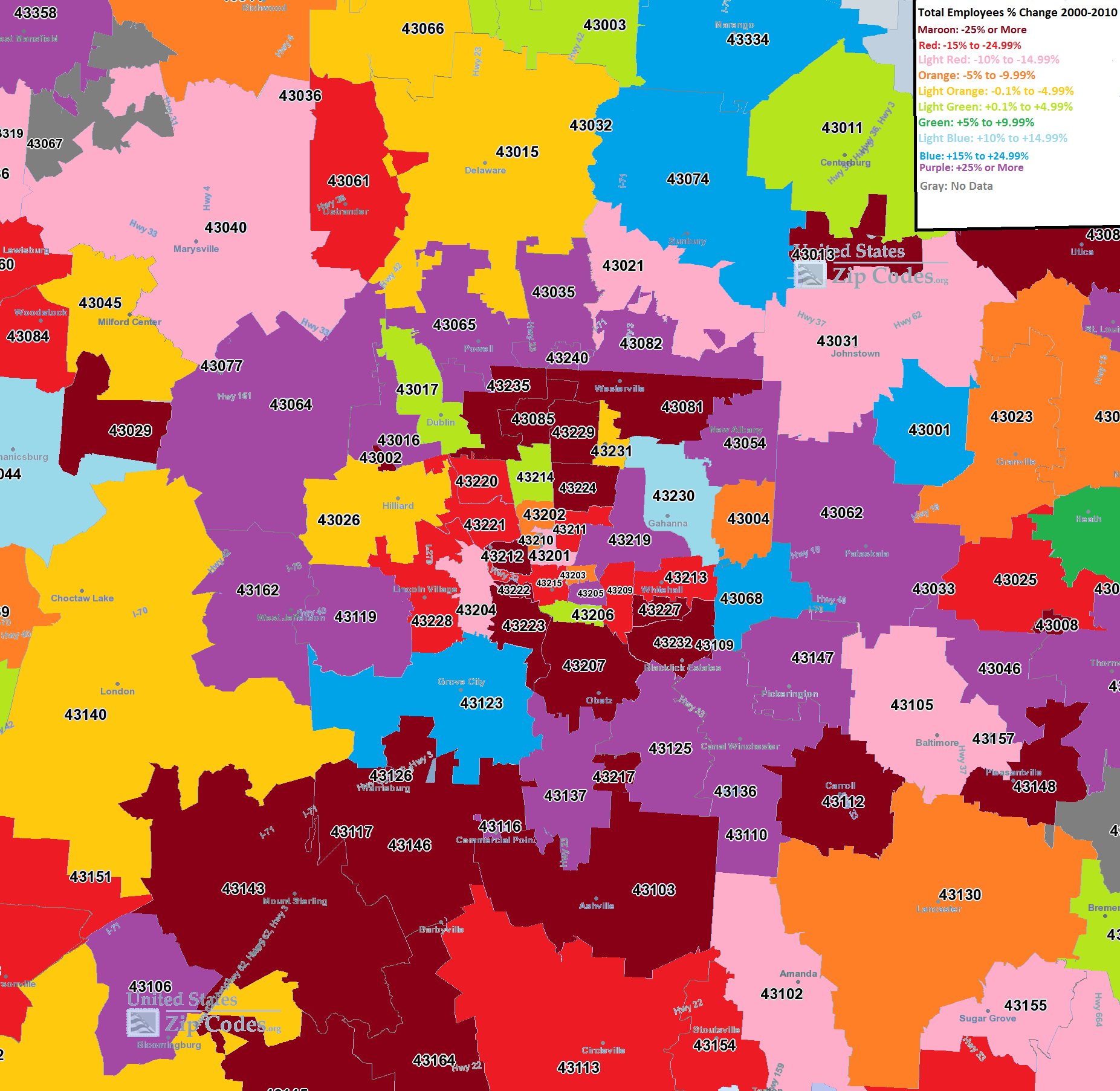

First, we have a map for the Columbus area that includes the % of of employees in a particular zip code from 2000-2010.

From this map, the urban areas of Columbus seem to have lost the most % of their employees the last decade, along with the far suburban and rural areas. The biggest growth was in the areas along and just outside of 270. This is an interesting map as it implies that the nearest suburban areas are attracting the most jobs, but that these suburbs are are both pulling from the inner core, but also from much further out.

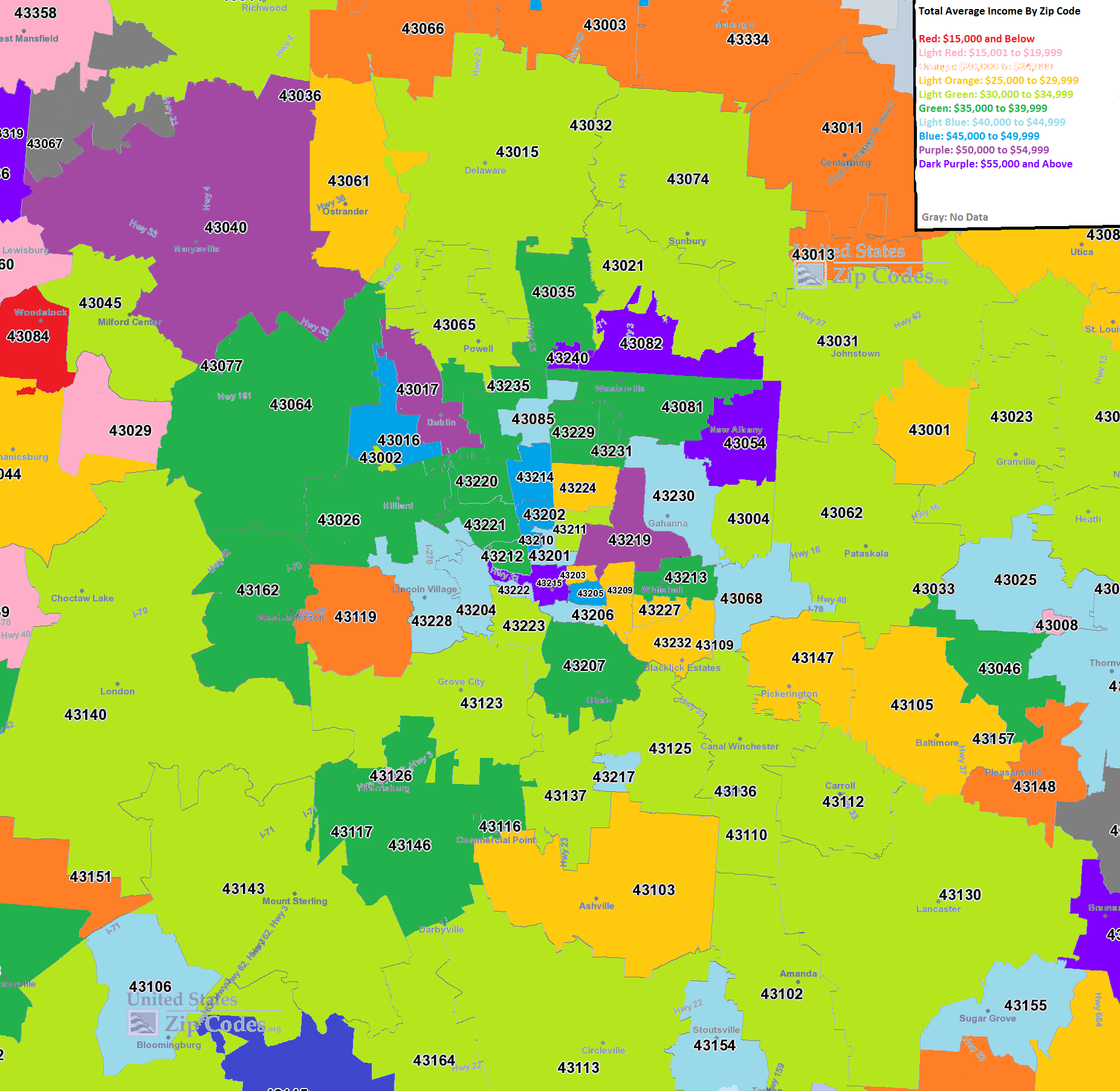

The second map is for average employee income by zip code.

What this map seems to show is that, while jobs may be moving to the I-270 suburbs, pay for those jobs is decidedly mixed across the city. Downtown, for example, averaged some of the highest incomes in the city. Other strong areas include parts of Westerville, New Albany and Dublin. Most of the High Street corridor was fairly strong as well. The lowest incomes were almost entirely in rural and far suburban areas.

Finally, the % change of average income from 2000-2010.

This map is also a mixed bag. Most of the area saw wage growth, but where it occurred the strongest was definitely all over the map. Some suburbs had good and bad, and so did the urban core areas.

So what’s all this mean? Well, certainly it means that the total # of jobs as far as growth shifted to the 270 suburbs the last decade, but at the same time, those jobs that remained in the core areas still grew in income. So it appears that the city is becoming richer about on par with the suburbs, at least the last 10 years. The question becomes, what happens the next decade? If urban trends continue the way they have the past few years (which these maps don’t really take into account), it is entirely possible that some of the job growth will move back inward towards the urban core.

To continue with local and national economic data, the US’ Bureau of Economic Analysis gives the option to look at cities, metro areas and other levels. Zip Code Maps gives population and demographic data in an interactive format.

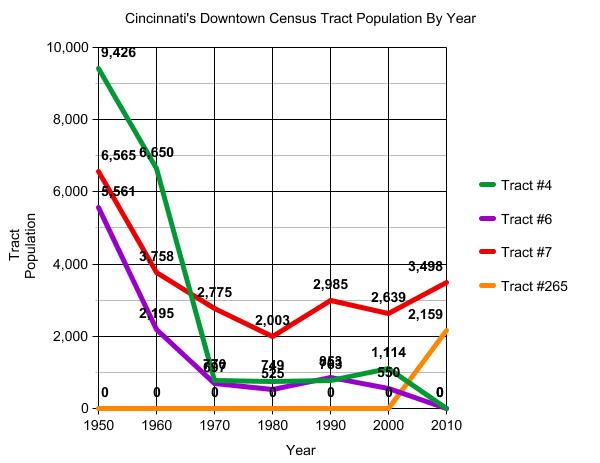

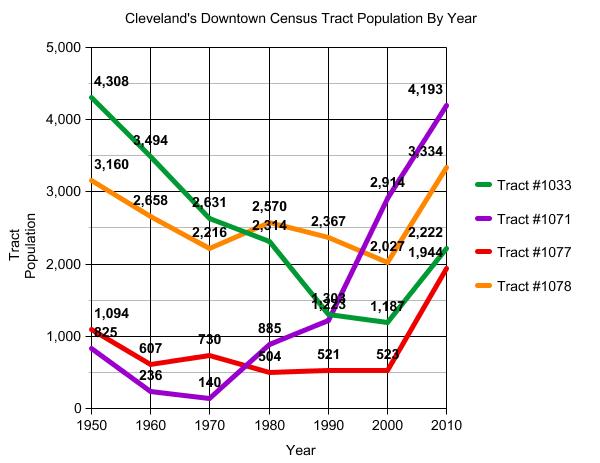

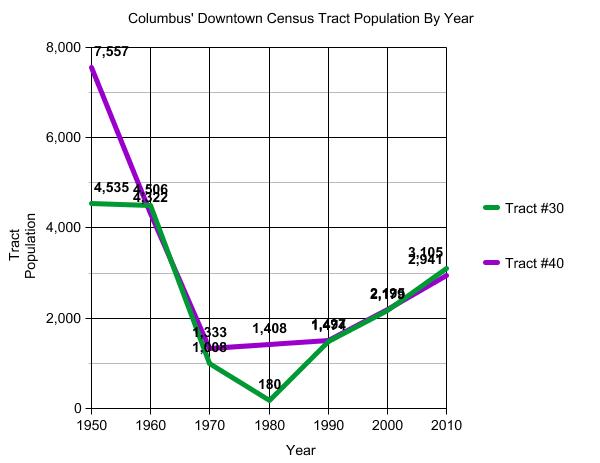

Yesterday, I talked about how the 1950 core population had changed the last 50 years. Today I want to focus just on the Downtown, or the Central Business District. This is a much smaller area for all three cities so there are far fewer tracts involved.

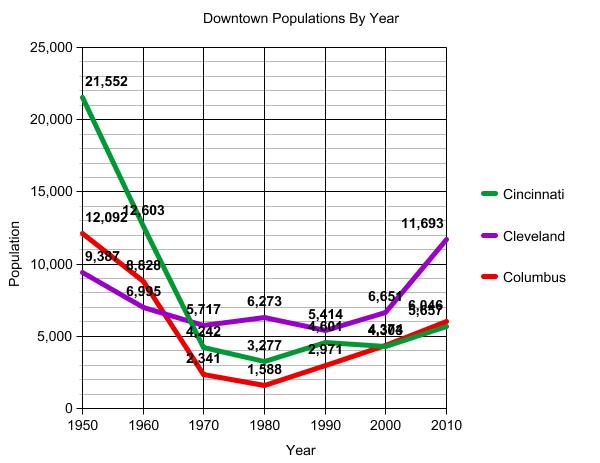

First, let’s look at the total Downtown populations since 1950. This graph, I think, will surprise most people. The first surprise is that downtown populations in 1950 were not nearly as high as most would have you believe. Cincinnati did have almost 22K people there, but even a city like Cleveland had less than 10K, and that was during the absolute peak of its city population. Another surprise is that Columbus was not always the lowest populated downtown and was more populated than Cleveland’s in 1950. Finally, the last surprise is that while all the downtowns are now growing, Columbus has regained 2nd place and Cleveland has seen the most growth so far.

What about tract trends for the downtowns? Well first, here are the population trends for each downtown. For Cincinnati, Tracts #4 and #6 were combined into #265 in 2010. So no city had a single Downtown tract that was not growing in 2010. This is good news.

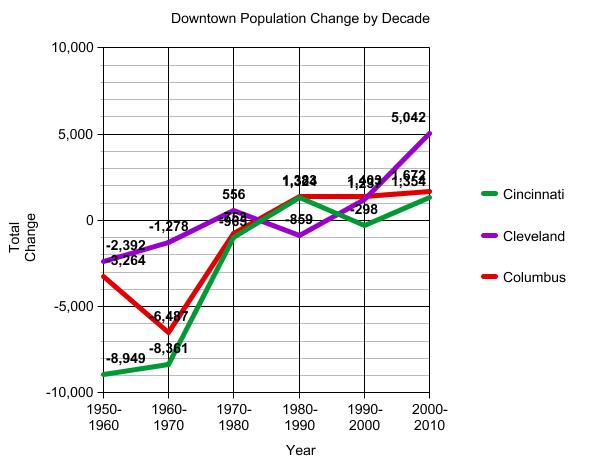

Here is the total population change by Downtown.

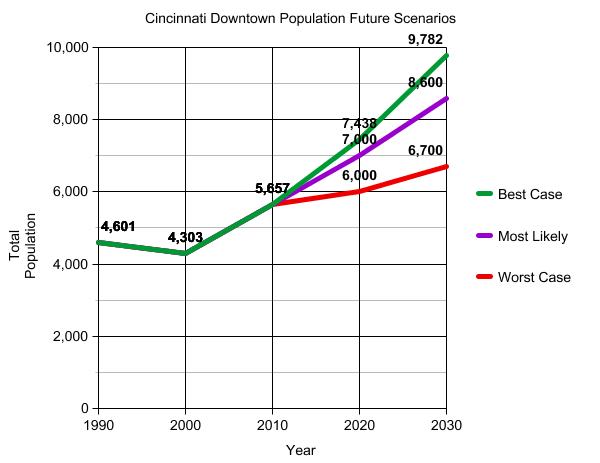

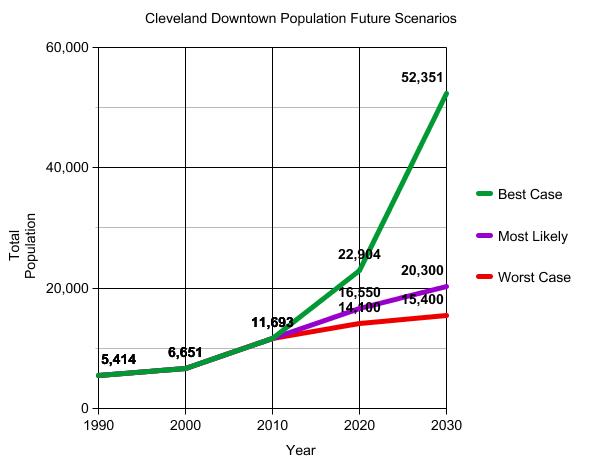

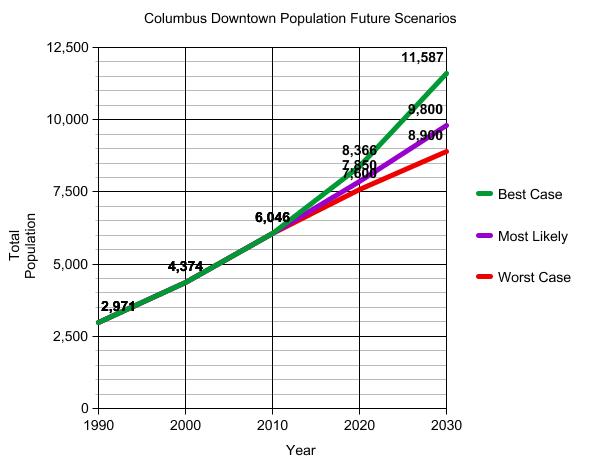

What about if these current trends continue, what might the downtown populations look like in 2020 or 2030?

If you think Cleveland has a very rapid rise for its Best Case scenario, that is because, to get the best case, I used the last decade’s growth rates and just assumed they would continue and compound growth. One of Cleveland’s tracts had a growth rate over 80% while another grew 271%. Still, while it’s the best case, it’s also highly unlikely to maintain growth rates that high for that long, so a more likely case is somewhere closer to Most Likely.

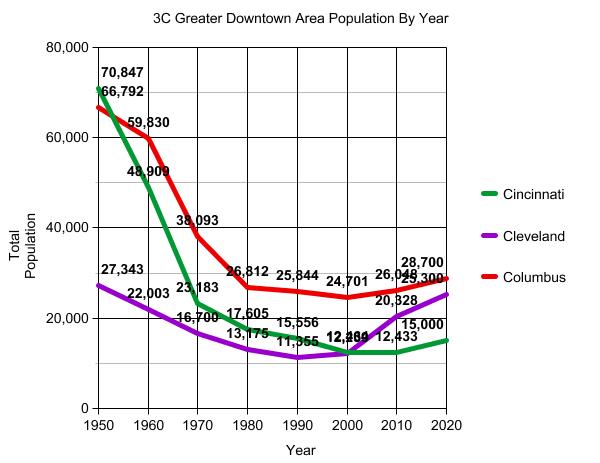

Finally, I wanted to look at more of the downtown area than just the central business district. “Downtown” for many includes more areas than that and may be a “Greater Downtown Area”, the measurement between the full 1950 boundaries and just the CBD.

Here are the tracts I considered to be the Greater Downtown area for each city.

And the graph for the population of these tracts since 1950 and a projection out to 2020. Cincinnati reached it’s lowest population for the past 60 years for this area in 2010, but just barely. It should be growing again by 2020, but I didn’t project the growth to be that high because it was still coming out of its lowest point. Cleveland’s greater downtown had the bottomed out in 1990 and had the fasted growth the past decade. Columbus managed to maintain the highest population in its greater downtown, bottomed out in 2000 and has grown since. However, not nearly as fast as in Cleveland. I expect Columbus to have better growth this decade and remain on top, but with Cleveland’s area closing the gap.

Columbus’ downtown has seen many many changes, especially over the last decade. Developments like the Arena District, Columbus Commons, the Scioto Mile and more have brought new life to the area. Dozens of new restaurants have opened the past year or two alone, and a new grocery store will be opening for area residents in February. More developments coming up include the Scioto River restoration project that will create acres of new Downtown park space and pathways, and the redevelopment of the Scioto Peninsula behind COSI should connect the two sides of the river. All of this had led to rising population, now approaching 7,000. More than 1,000 residential units are currently under construction and more is on the way. So the question I was wondering is how has population been changing not only in Columbus’ downtown, but in comparison to Cleveland and Cincinnati. Both of those cities have also seen major projects in their downtown cores and are seeing an uptick in their downtown populations.

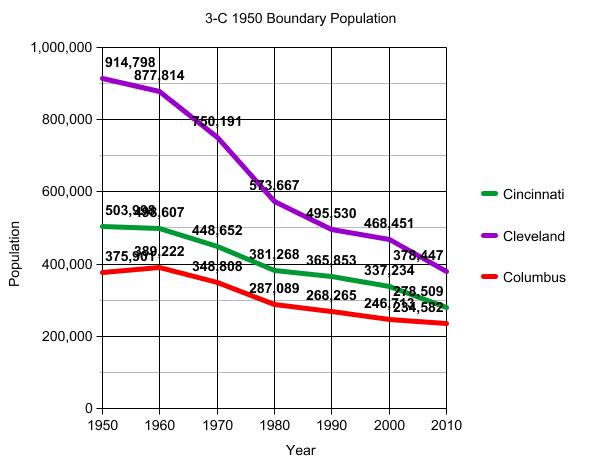

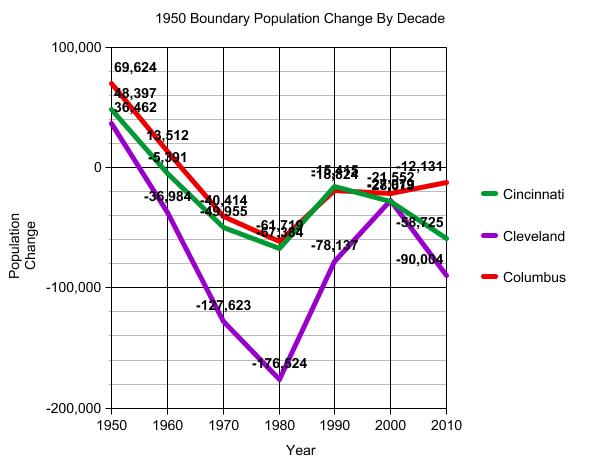

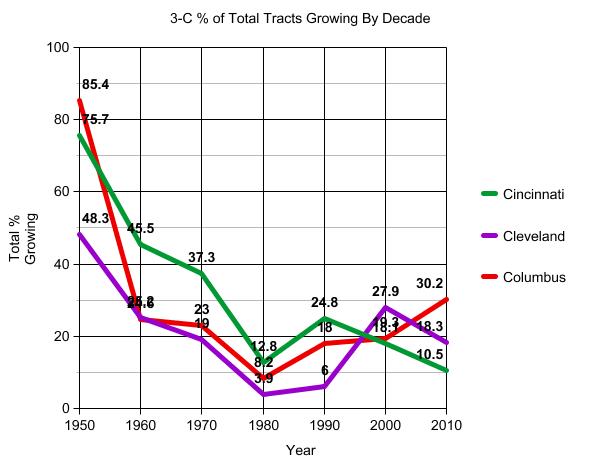

First, I examined the 1950 city limits for all three cities. This was the last census year before sprawl really took hold and changed the city dynamics and growth patterns. 1950 is also when most cities in Ohio reached their peak urban population, so I thought it would be interesting to see how those old boundaries had changed over the years. I went to the US census website and began to look up all the census tracts that existed in each city in 1950. Those would represent my base area that I would use to see the changes in the city core. All of the 3-Cs have grown beyond those 1950 boundaries, especially Columbus, but these areas were the hardest hit when the urban decline came the last 50-60 years while the suburbs grew. The results are both sobering and hopeful.

So what do these numbers show? Well, it’s clear that all 3 cities had urban core population declines the past 60 years just like just about every other city in the nation did. This was mostly a result of the suburban movement. In Cleveland, the rate of loss had gradually been slowing down since the 1970s, but suddenly skyrocketed again in the 2000s. I’m not sure what exactly caused this. The double recessions made it more difficult for people to move, so if anything, the losses should’ve not accelerated. Cleveland lost over 90,000 people in its urban core from 2000-2010, the highest lost by % and total of any Ohio city. In Cincinnati, population loss had peaked in the 1970s and the rate of loss fell substantially the following decade. However, the past 2 decades have actually seen a gradual acceleration of losses. The 2000-2010 period saw the second biggest total loss for the urban core. For Columbus, it’s been the opposite picture. Like the other 2-Cs, losses peaked in the 1970s. Since then, the urban core losses have been in gradual decline. The 2000-2010 period had the smallest rate and total loss of any decade the past 60 years.

So interesting results, but these numbers don’t show any trends of what’s going on inside the 1950 boundaries, especially not the relatively small part that would be the downtowns. So let’s break the numbers down to the tract level.

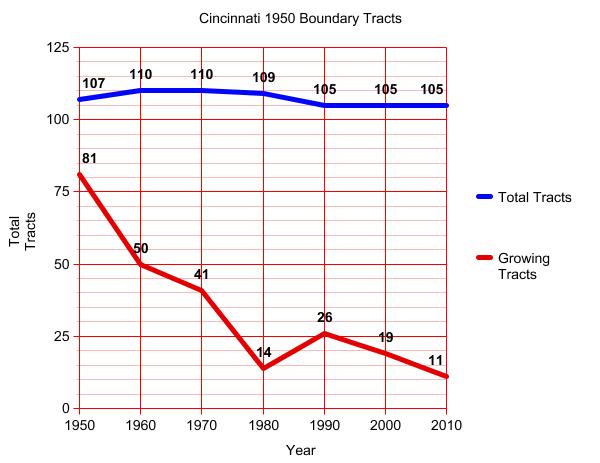

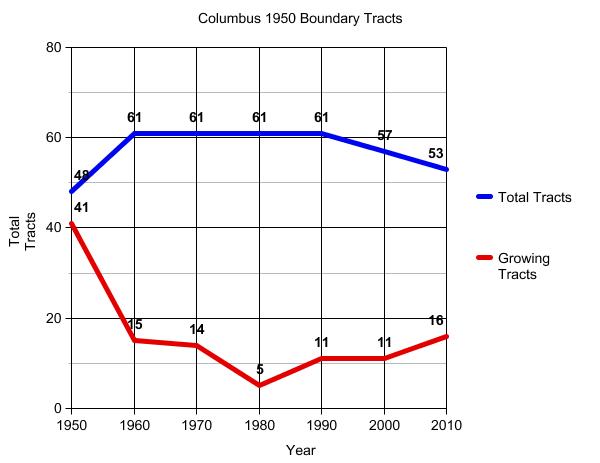

# of Tracts in 1950* Cincinnat: 107 Cleveland: 201 Columbus: 48

*The number of tracts changed from 1950 on as some were split or consolidated. This made it more complicated, but luckily the Census gives lists on how tracts changed over time, so one can figure out what tract became what and reasonably keep up with the same boundaries that existed in 1950. So with this breakdown, we can see more of the trends within the 1950 boundaries. In Cincinnati, a long decline was followed by a recovery in 1990, only to have the next 20 years show an increasing decline. The 2010 census showed the fewest number of tracts growing on record. This is the worst performance of the 3-Cs. Cleveland also had a steep decline followed by a recovery, but it too declined more at the last census, but not nearly to the low point it reached in the 1970s and 1980s.

Meanwhile, Columbus also faced an initial steep decline and barely had any tracts growing during the 1970s. Since then, the trend has been up. The 16 growing tracts in 2010 were the highest since the 1940s. This is the best performance of the 3-Cs, and Columbus had the highest % of growing tracts in its core. Still, those 16 represent less than 1/3rd of the total tracts within the 1950 boundaries. So while there appears to be recovery ongoing in Columbus, especially compared to Cleveland and Cincinnati, it’s not where it needs to be.

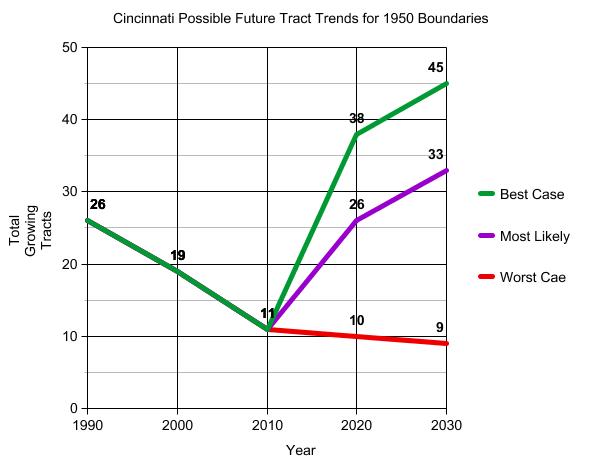

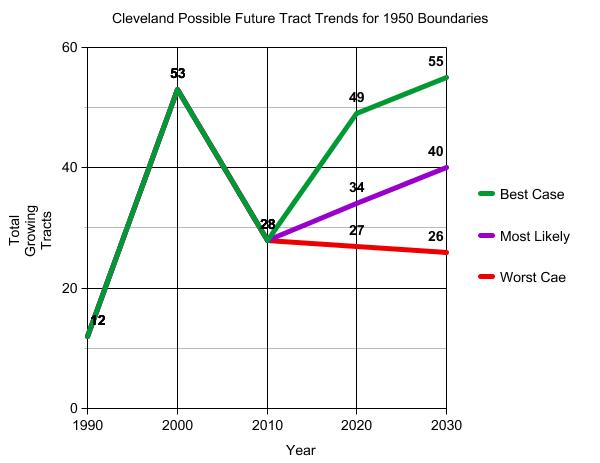

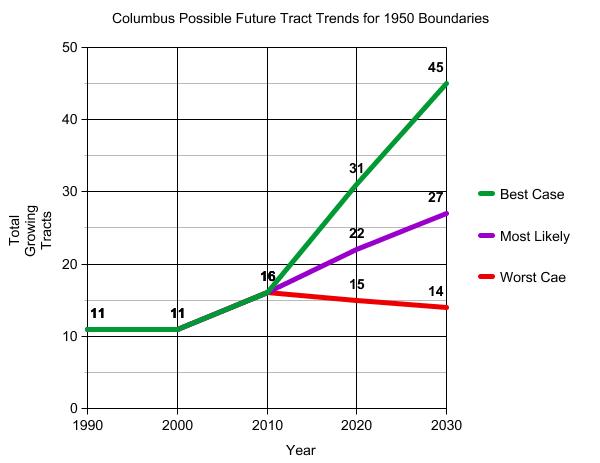

So let’s look to the future. All these tracts are trending in certain directions themselves. While they may be losing now, they may be trending toward an eventual gain, and vice versa. If we follow the trends ongoing for the urban core tracts, where might the picture look like in say, 2020?

Tract Trends for Those Tracts Growing in Population in 2010 Trends are listed from what, in my opinion are the most positive to the most negative.

Growing in both 2000 and 2010, but Growth Accelerating Over Time and % of Total Tracts Cincinnati: 0- 0% Cleveland: 7- 4.6% Columbus: 5- 11.3%

Shrinking in 2000 but Growing in 2010 and % of Total Tracts Cincinnati: 10- 9.5% Cleveland: 20- 13.1% Columbus: 10- 18.9%

Growing in both 2000 and 2010, but Growth Slowing Over Time and % of Total Tracts Cincinnati: 1- 1.0% Cleveland: 1- 0.7% Columbus: 1- 1.9%

Shrinking in both 2000 and 2010, but Loss Slowing Over Time and % of Total Cincinnati: 28- 26.7% Cleveland: 21- 13.7% Columbus: 15- 28.3%

These tracts are those most likely to switch to positive growth come 2020. This is arguably one of the more positive trends and may deserve to be bumped a bit higher on the list.

Growing in 2000 but Shrinking in 2010 and % of Total Cincinnati: 18- 17.1% Cleveland: 42- 27.5% Columbus: 5- 9.4%

Shrinking in both 2000 and 2010, but Loss Accelerating and % of Total Cincinnati: 48- 45.7% Cleveland: 93- 60.8% Columbus: 17- 32.1%

These are the worst of the worst tracts, likely representing the most declined parts of the urban core. It’s pretty surprising to see that almost 2/3rds of Cleveland’s tracts are in this condition.

The tract trends paint a very interesting picture about each city’s urban core future. If we expanded these trends to the next census in 2020, this is what you might see.

All this information, however, deals with the entire urban core. What about just the Central Business Districts, or the downtown areas for each city? In , I will examine those numbers and trends for the very heart of these cities.

In a first of its kind, this is the Columbus housing market update for December 2012. In it, the local housing market will be detailed by categories such as most expensive market, market listing rankings and more.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

Top 15 Most Expensive Locations By Median Sales Price in December 2012 1. New Albany: $535,000 2. New Albany Plain LSD: $397,450 3. German Village: $376,000 4. Grandview Heights: $362,500 5. Powell: $354,950 6. Dublin: $343,600 7. Granville CSD: $330,000 8. Bexley: $325,000 9. Upper Arlington CSD: $319,500 10. Olentangy LSD: $315,000 11. Big Walnut LSD: $306,250 12. Dublin CSD: $271,500 13. Worthington: $$270,000 14. Buckeye Valley LSD: $259,000 15. Sunbury: $253,000

New Albany was by far the most expensive local market around Columbus.

Top 15 Least Expensive Locations by Median Sales Price in December 2012 1. Obetz: $80,100 2. Hamilton LSD: $80,100 3. Whitehall: $85,950 4. Newark CSD: $86,900 5. Lancaster CSD: $103,000 6. Jefferson LSD: $123,000 7. London CSD: $124,000 8. Groveport Madison LSD: $125,900 9. Reynoldsburg CSD: $125,950 10. Columbus CSD: $129,900 11. South-Western CSD: $131,000 12. Columbus: $140,026 13. Jonathan Alder LSD: $150,000 14. Minerva Park: $159,500 15. Grove City: $160,950

Southern and eastern suburbs tend to perform best on this list, as well as Columbus itself.

Overall Market Median Sales Price in December 2012: $158,645

Top 15 Locations with the Highest Median Sales Price % Growth Between December 2011 and December 2012 1. Whitehall: +69.5% 2. Circleville CSD: +64.9% 3. Sunbury: +63.0% 4. Jefferson LSD: +53.5% 5. Big Walnut LSD: +44.1% 6. Canal Winchester CSD: +40.9% 7. Westerville: +29.8% 8. Westerville CSD: +27.3% 9. Powell: +25.4% 10. Pataskala: +24.0% 11. Olentangy LSD: +23.5% 12. Gahanna Jefferson CSD: +21.8% 13. Grandview Heights: +21.2% 14. Granville CSD: +20.0% 15. Pickerington: +17.7%

Top 15 Locations with the Lowest Median Sales Price % Growth Between December 2011 and December 2012 1. London CSD: -53.5% 2. Obetz: -38.3% 3. Hamilton LSD: -27.1% 4. Jonathan Alder LSD: -25.2% 5. Buckeye Valley LSD: -23.0% 6. Reynoldsburg CSD: -18.7% 7. Hilliard: -17.7% 8. Lancaster CSD: -17.6% 9. Grove City: -15.3% 10. Dublin CSD: -12.8% 11. Johnstown Monroe LSD: -10.8% 12. Upper Arlington CSD: -8.5% 13. Newark CSD: -8.1% 14. Dublin: -7.1% 15. South-Western CSD: -6.4%

Overall Market Median Sales Price % Change December 2011 vs. December 2012: -0.3%

Top 10 Locations with the Most New Listings in December 2012 1. Columbus: 829 2. Columbus CSD: 544 3. South-Western CSD: 136 4. Olentangy LSD: 122 5. Westerville CSD: 100 6. Hilliard CSD: 94 7. Dublin CSD: 89 8. Worthington CSD: 66 9. Dublin: 64 10. Pickerington LSD: 60

Top 10 Locations with the Fewest New Listings in December 2012 1. Valleyview: 0 2. Lithopolis: 1 3. Sunbury: 2 4. Minerva Park: 2 5. Obetz: 3 6. Johnstown Monroe LSD: 5 7. Jefferson LSD: 8 8. German Village: 8 9. Hamilton LSD: 8 10. Whitehall: 11 11. Granville CSD: 12

Total New Listings in the Columbus Metro in December 2012: 2,002 Overall Metro New Listings % Change December 2011-December 2012: +10.5%

Overall, prices are slightly down as supply is currently outstripping demand.

For more information on the local market, go here: Columbus Realtors