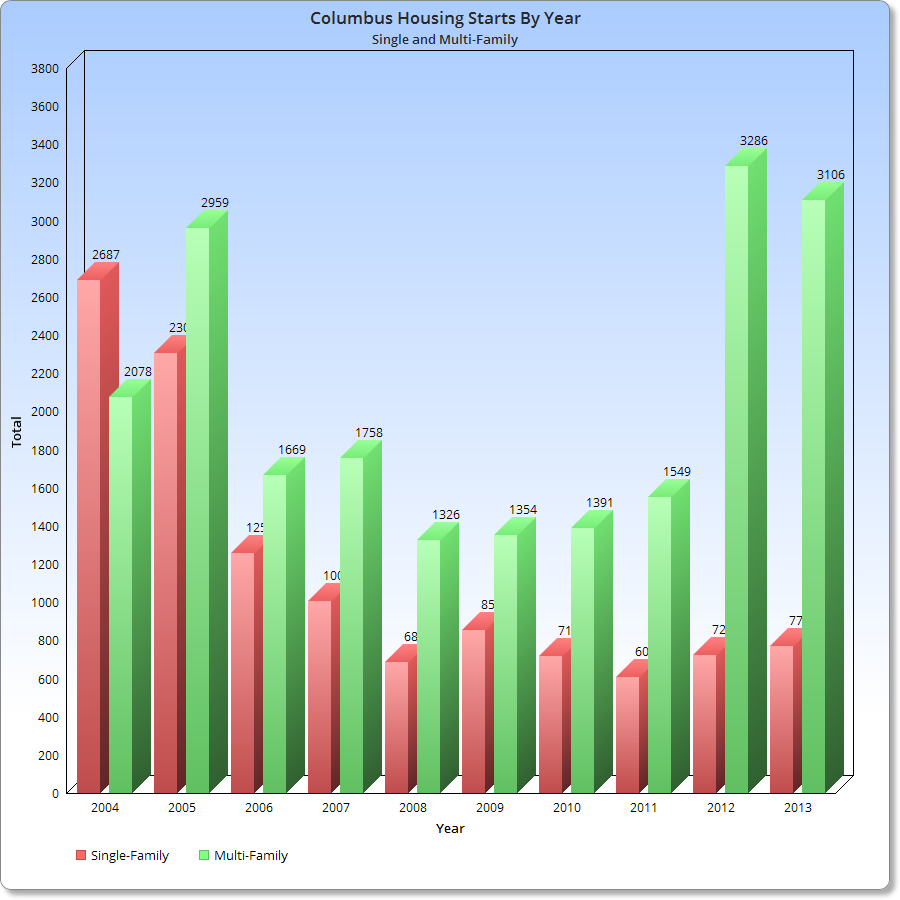

I’m not a complainer… or at the very least, I don’t prefer to be. That said, there are simply times where negativity makes perfectly logical sense, and where it can serve a real purpose for true positive change. That is arguably the case now, with the a very poor decision about the Columbus Convention Center. I’ve not posted too much on my personal views regarding development, but recent events have prompted me to give some of them on this particular project.

Back in March, it was revealed that the Greater Columbus Convention Center leadership had asked the local development community to come up with ideas for a potential expansion project for the convention center itself. The building was designed by famed 1980s and early 1990s architect Peter Eisenman (who also did the Wexner Center for the Arts), and began construction in 1989 and completed in 1990. Originally, the building included 1.4 million square feet of space, with a large parking lot occupying the southeast corner of the Goodale/N. High Street intersection.

In 1999, an expansion pushed the structure north nearly to Goodale, but left enough space for a small plaza there.

So even after the initial construction of the original building, there were obvious problems with the design, not least of which was the pastel color scheme better suited for Miami Beach. The building simply didn’t have any street-level presence. Beyond a few entrances, the convention center’s design essentially created a block-long wall along High Street. There was no ground floor retail, no restaurants and no pedestrian interaction whatsoever. Back in 1989, this was just fine and dandy, because no one really cared about that and hadn’t since the days before WWII. Cities had become showplaces and for big buildings and massive surface parking lots that didn’t actually bring anyone to live there. There was no reason to walk on the streets of the city, and architects certainly didn’t think it was necessary to build for that purpose. The suburbs were the real future, blah blah blah. Everyone knows that story.

Since 1999, the neighborhood around the convention center has been rocketing upward in popularity. The nearby Arena District continued to grow and add development, and the Short North continued to rapidly revitalize and is now the city’s hottest neighborhood. For the past few years, there has been a push to attract more business to Columbus via the center and to highlight all the nearby amenities. To that end, the 12-story, 500+ room Hilton was completed across the street in 2012. The $140 million structure was built with public dollars, as a private developer did not step forward when the idea was put forth. The project was somewhat speculative, as the demand for hotel space in the city was not particularly high enough to warrant the construction (a good reason why private development hadn’t shown up), but because the city understood that hotel space was part of the key to attract bigger and better convention events, the hotel went up and Hilton came in to run the space.

The gamble seemed to be paying off, and in January, the Columbus Dispatch came out with an article about the hotel’s success. In the article, there was even the mention of adding even more hotel space, possibly up to 1,000 additional rooms, at some point in the near future.

So when the convention center authority announced it was searching for ideas for a new expansion project, that reality seemed to be taking place. In late March, there was this bit of news. Four separate proposals had been submitted by private developers on ideas to develop the north end of the convention center, along with the surface parking lot north of Goodale behind the 670 retail cap. The most prominent idea came from Wagenbrenner, with a pair of 15-story, mixed-use towers that would’ve included more than 100 residential units, hotel and event space, and ground-floor retail along High Street, an element the original building severely lacked.

Wagenbrenner Development’s proposal.

Wagenbrenner Development’s proposal, looking southeast from High and Goodale.

Another proposal from Kaufman was far more modern, but still retained mixed-use elements.

The Kaufman proposal, looking east on Goodale.

In Wagenbrenner’s case, a hotel chain had already stepped forward interested in running the hotel aspect of the project, and there seemed little doubt that one of the proposals would move forward, based on quotes from the convention center authority and their stated goal for a “big idea” sort of project moving forward. The selection of the design would be announced in a few month’s time.

So what was the result of all that? On June 12th, 2014, an article in the Dispatch came out detailing a renovation and expansion project for the convention center.

The problem was that the article did not mention any mixed-use project whatsoever. Instead, it called for a general total-building renovation and a small 30,000 sf expansion and entranceway into the plaza space at the southeast corner of High and Goodale. Additionally, an 800-space parking garage would be built in the surface lot behind the 670 cap.

Wait, what?? When the article initially came out, there was confusion by many in the development-following community on just what was going on. Part of the confusion stemmed from the fact that the convention center authority had already announced a renovation project just 2 weeks prior to the release of the information on the mixed-use expansion project. That announcement had mentioned only a $30 million renovation, not the much larger one announced on June 12th. There had also been mention previously of the garage project, back in late 2013. In that discussion, the garage was being looked at to get ground-floor retail, especially closer to High, to take advantage of the neighborhood’s high walkability and retail success.

So at first, it was assumed that the garage and renovation project was a separate issue from the larger proposed expansion, but the article on June 12th specifically mentioned the very same land that the proposed mixed-use towers would’ve used. The following day, on June 13th, the Dispatch came out with a second article about the $125 million renovation/expansion project, and in it near the bottom, was this damning paragraph:

Jennison said the expansion of the convention center rules out earlier ideas of adding shops and residences to the north end of the facility, including the possibility of more hotel space. The authority’s board sought proposals for such a project earlier this year before ultimately ruling them out.

Suddenly, the 2-tower project had been swept under the rug and abandoned. Worse, it had been abandoned in favor of new carpets/fresh paint, a glorified 2-story entrance on Goodale, and a 1970s parking garage with no retail at all.

The parking garage proposal on Goodale behind the 670 retail cap, part of the convention authority’s new plan.

To say that there was some disbelief that such a decision had been made is putting it mildly. Across development forums, and even on the Dispatch articles themselves, the negative reaction was swift and universal. How and why had such a promising proposal for the convention center turned into the height of mediocrity? And why had potential fully private or a private/public funded project turned into a 100% publicly funded fiasco? The answer, it seems, is likely staring us in the face: The Hilton Hotel. Though it hasn’t been confirmed either way, there is an element of suspicion against the Hilton for obvious reasons. The Hilton is publicly financed and was publicly built. To have a private company build a competing hotel may have taken away business, and the convention authority was not interested in allowing competition for a public enterprise. There are precious few other logical reasons why the convention authority would actively seek private investment only to toss those proposals out a few months later in favor of a project that had no competing elements to it.

Worse still, the convention authority knows it’s a terrible plan in comparison. On June 15th, yet another article on the project appeared in the Columbus Dispatch.

In it, the idea is pushed forth that the renovation plan will be transformative, and will keep Columbus competitive for convention business. The problem is that it’s neither transformative nor competitive. Granted, the convention center is in need of renovations, as much of the interior is dated. But to spend $125 million on that renovation, combined with a laughably bad expansion/garage rather than actually going with, at the very least, a partially privately-funded project that would’ve actually improved Columbus’ competitiveness along with adding much needed pedestrian access and excitement to the intersection in question… well, it’s insanity. And the 3rd article only suggests that the convention authority is well aware of the overwhelmingly negative reaction to their plan and are attempting to justify it as much as possible. Only there can be no real justification. Bad decisions remain bad decisions. Whether this one was made to prevent competition or is simply an example of being out of touch with a stated goal, the convention center authority has made one of the worst decisions in Columbus development history… and that was after the city allowed Union Station to be demolished. Shame on them.