The housing market update May 2014 report for the Columbus area, courtesy of Columbus Realtorscontinued to show the 5-month long trend of sales being down. As with the previous 4 months, the main reason was high demand coupled with historically low supply.

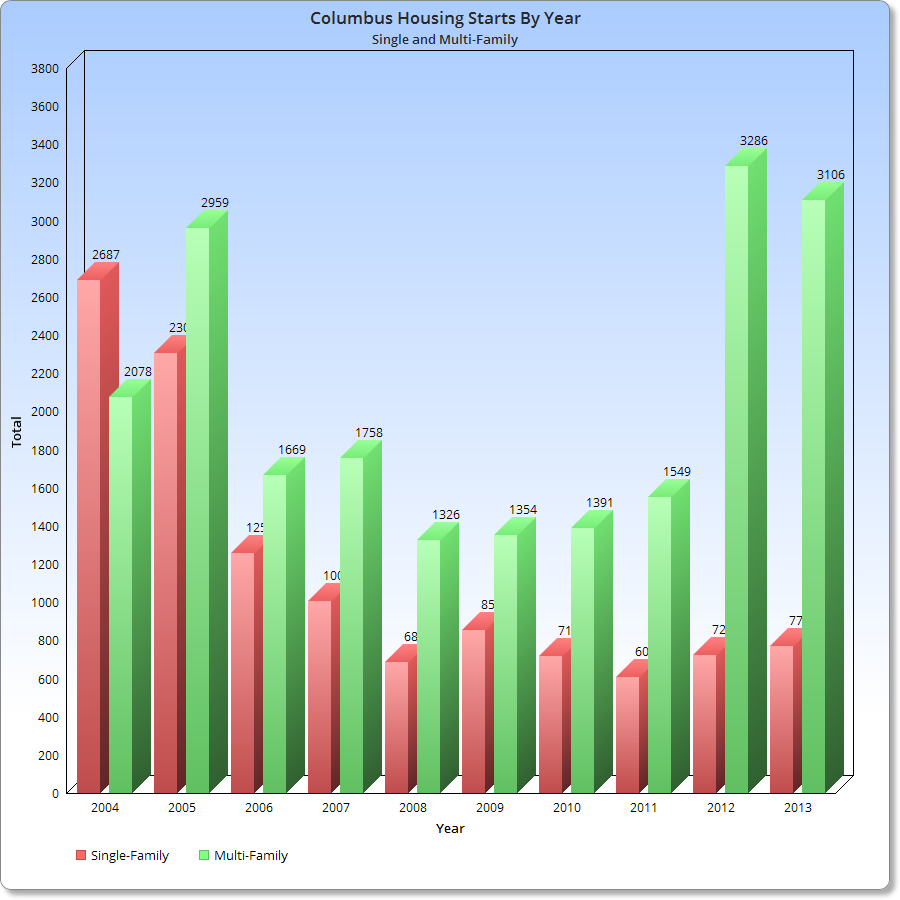

As for when this situation may change seems hard to guess. The rate of construction for single family homes shows no real signs of improving anytime soon, while renting continues to be the dominant choice right now.

Top 10 May 2014 Sales Totals

1. Columbus: 1,008

2. Grove City: 81

3. Clintonville: 73

4. Dublin: 73

5. Westerville: 67

6. Reynoldsburg: 59

7. Hilliard: 58

8. Upper Arlington: 55

9. Gahanna: 45

10. Pickerington: 36

Top 10 May 2014 Sales Increases over May 2013

1. New Albany: +35.3%

2. Pataskala: +35.0%

3. Obetz: +33.0%

4. Downtown: +30.0%

5. Grove City: +20.9%

6. Westerville: +3.1%

7. Pickerington: -2.7%

8. Hilliard: -4.9%

9. Columbus: -11.6%

10. Reynoldsburg: -11.9%

Top 10 Year-to-Date Sales Through May 2014

1. Columbus: 3,716

2. Dublin: 261

3. Grove City: 258

4. Clintonville: 248

5. Westerville: 229

6. Upper Arlington: 220

7. Reynoldsburg: 209

8. Hilliard: 187

9. Gahanna: 150

10. Pickerington: 108

Top 10 Year-to-Date Increases Through May 2014 Over 2013

1. Obetz: +118.2%

2. New Albany: +11.3%

3. Pataskala: +8.7%

4. Grove City: +5.3%

5. Reynoldsburg: +1.0%

6. Westerville: -3.0%

7. Clintonville: -5.0%

8. Downtown: -8.0%

9. German Village: -8.8%

10. Worthington: -9.2%

Average Sales May 2014

Urban: 114

Suburban: 49.6

Urban without Columbus: 25

Average % Change May 2014 vs. May 2013

Urban: -13.1%

Suburban: +1.4%

Urban without Columbus: -13.3%

Average YTD Sales Through May 2014

Urban: 419

Suburban: 167

Urban without Columbus: 89

Average YTD % Change YTD Through May 2014

Urban: -1.7%

Suburban: -6.0%

Urban without Columbus: -1.1%

Top 10 Average Sales Price May 2014

1. New Albany: $549,217

2. Dublin: $400,121

3. Bexley: $355,732

4. Upper Arlington: $345,156

5. German Village: $290,299

6. Downtown: $272,927

7. Worthington: $258,483

8. Grandview Heights: $238,333

9. Hilliard: $231,340

10. Westerville: $214,817

Top 10 Average Sales Price % Change May 2014 vs. May 2013

1. Obetz: +42.2%

2. Upper Arlington: +22.1%

3. Dublin: +18.6%

4. Westerville: +15.3%

5. Minerva Park: +14.5%

6. Grandview Heights: +12.5%

7. Reynoldsburg: +11.3%

8. Clintonville: +10.7%

9. Columbus: +9.4%

10. Pickerington: +9.3%

Top 10 Average Sales Prices YTD Through May 2014

1. New Albany: $491,395

2. Dublin: $356,009

3. Upper Arlington: $334,705

4. Bexley: $322,383

5. Downtown: $303,479

6. German Village: $297,917

7. Worthington: $256,332

8. Grandview Heights: $245,403

9. Hilliard: $222,793

10. Westerville: $207,854

Top 10 Average YTD Sales Price % Change Through May 2014 vs. 2013

1. Obetz: +50.8%

2. Grandview Heights: +20.5%

3. Pataskala: +15.9%

4. Grove City: +11.7%

5. Dublin: +11.6%

6. Pickerington: +11.3%

7. Westerville: +10.7%

8. Columbus: +9.7%

9. Worthington: +9.6%

10. Reynoldsburg: +9.2%

Average Sales Price May 2014

Urban: $221,969

Suburban: $240,310

Urban without Columbus: $229,903

Average Sales Price Change May 2014 vs. May 2013

Urban: +3.9%

Suburban: +4.5%

Urban without Columbus: +3.3%

Average Sales Price YTD Through May 2014

Urban: $217,709

Suburban: $227,022

Urban without Columbus: $226,296

Average Sales Price % Change YTD Through May 2014

Urban: +9.4%

Suburban: +8.0%

Urban without Columbus: +9.3%

Top 10 Fastest Selling Markets May 2014 (Based on Average # of Days for Listings to Sell)

1. Minerva Park: 7

2. Grandview Heights: 12

3. Upper Arlington: 19

4. Worthington: 27

5. Bexley: 31

6. Clintonville: 41

7. Westerville: 41

8. Dublin: 42

9. Obetz: 50

10. Hilliard: 52

Top 10 Fastest Selling Markets YTD Through May 2014

1. Minerva Park: 42

2. Obetz: 44

3. Worthington: 44

4. Upper Arlington: 47

5. Grandview Heights: 49

6. Hilliard: 50

7. Westerville: 55

8. Clintonville: 56

9. Pickerington: 58

10. Dublin: 62

Average # of Days Before Sale, May 2014

Urban: 41.7

Suburban: 63.1

Urban without Columbus: 39.9

Average # of Days Before Sale YTD Through May 2014

Urban: 61.4

Suburban: 72.0

Urban without Columbus: 60.0

Top 10 Lowest Market Housing Supplies May 2014 (Based on # of Months to Sell all Listings)

1. Worthington: 1.3

2. German Village: 1.7

3. Grandview Heights: 1.7

4. Westerville: 1.9

5. Clintonville: 2.0

6. Minerva Park: 2.2

7. Gahanna: 2.3

8. Hilliard: 2.3

9. Obetz: 2.4

10. Upper Arlington: 2.5

A healthy housing supply is considered to be around 5-6 months. Anything less than 3 months is considered very low.

Average # of Months to Sell All Listings, May 2014

Urban: 2.5

Suburban: 3.2

Urban without Columbus: 2.5

Average % Change of Single-Family Home Sales May 2014 vs. May 2013

Urban: -18.4%

Suburban: +4.6%

Urban without Columbus: -18.8%

Average % Change of Single-Family Home Sales YTD Through May 2014 vs. YTD 2013

Urban: -8.0%

Suburban: -6.1%

Urban without Columbus: -7.8%

Average % Change of Condo Sales May 2014 vs. May 2013

Urban: +26.3%

Suburban: -20.0%

Urban without Columbus: +29.0%

Average % Change of Condo Sales YTD Through May 2014 vs. YTD 2013

Urban: +22.0%

Suburban: -12.0%

Urban without Columbus: +24.0%