The Housing Market Update January 2023 data, the first of the new year, from Columbus Realtors showed that home sales and overall supply continued to decline, helping to ensure most areas saw continued increases in median prices.

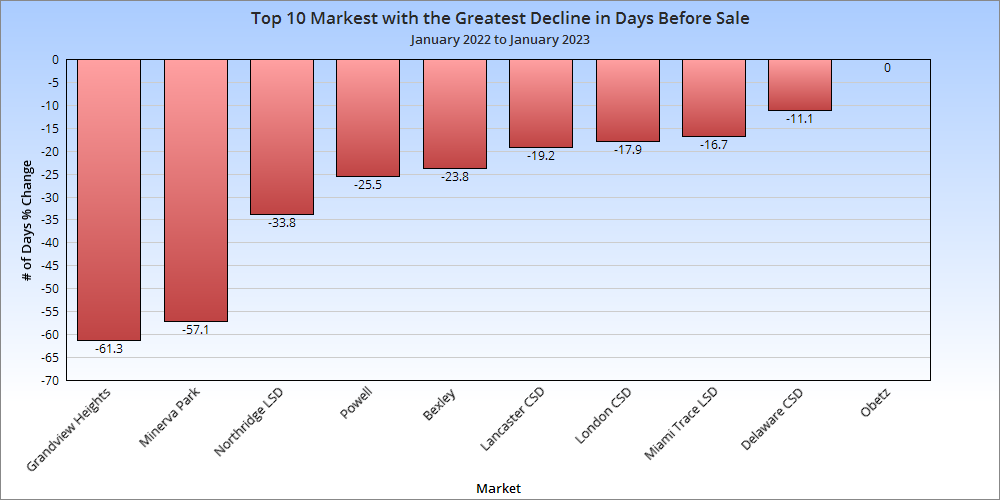

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

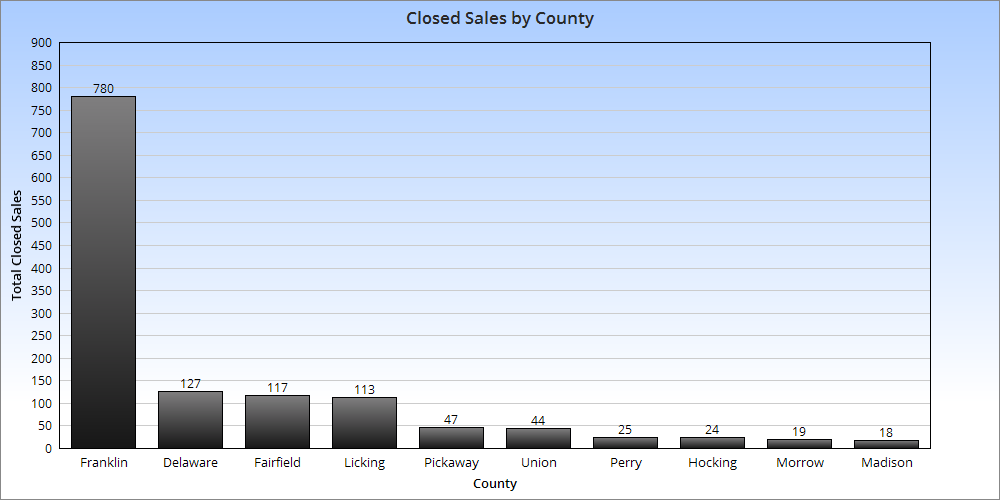

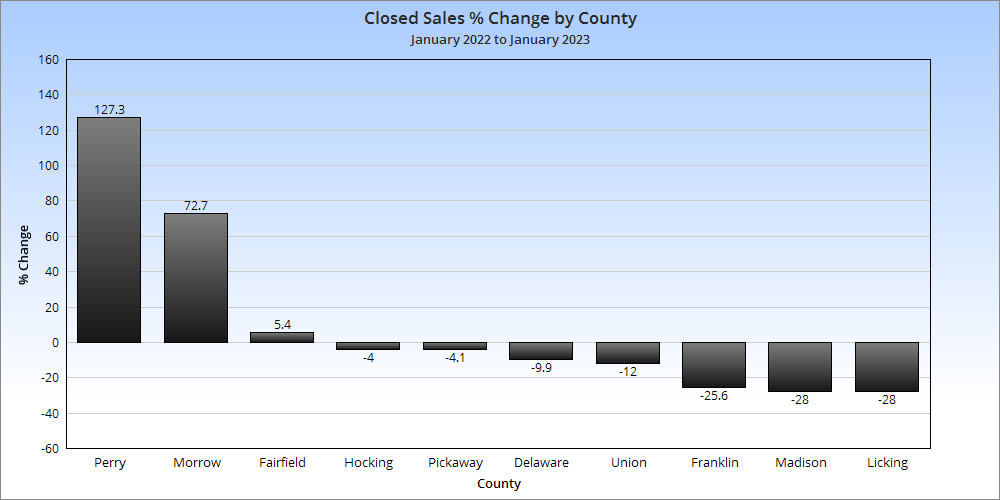

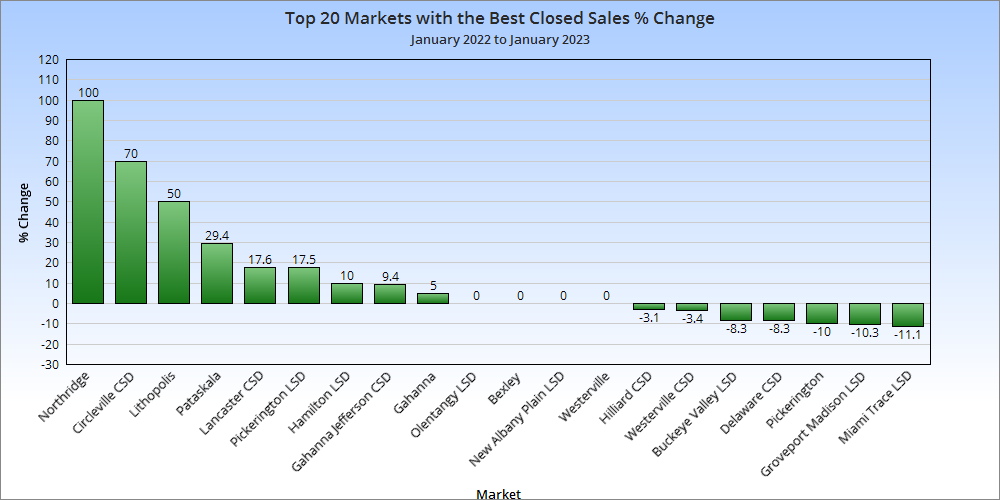

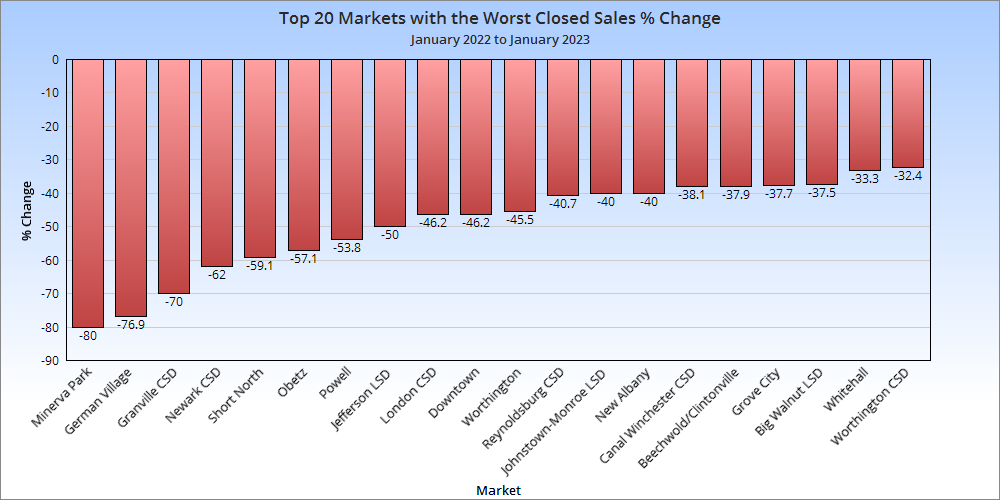

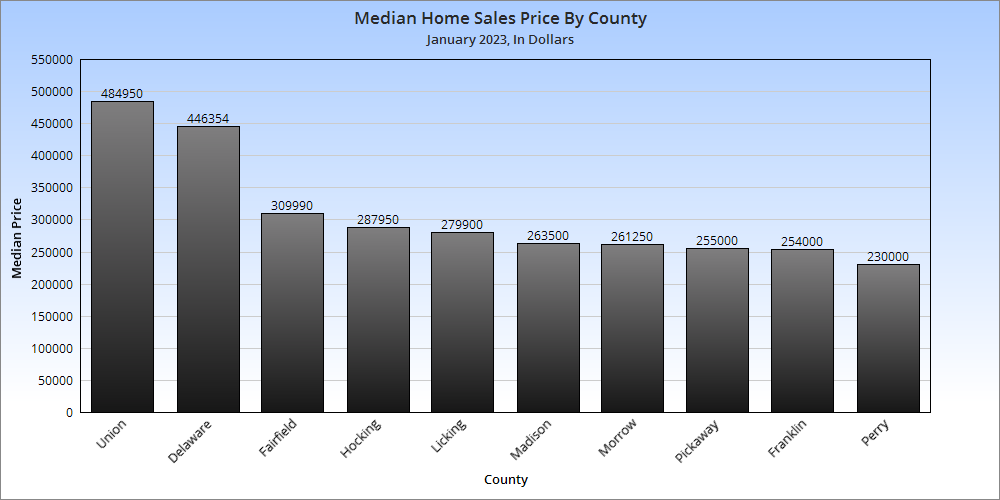

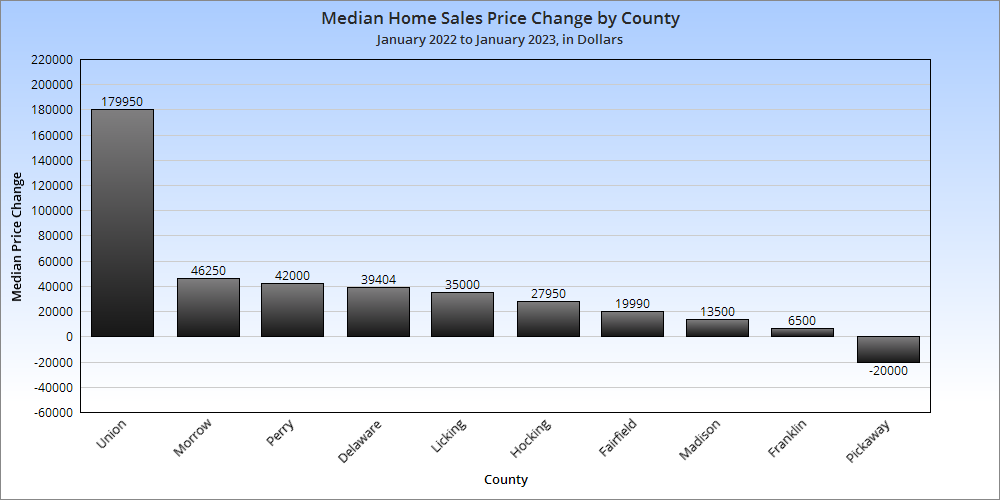

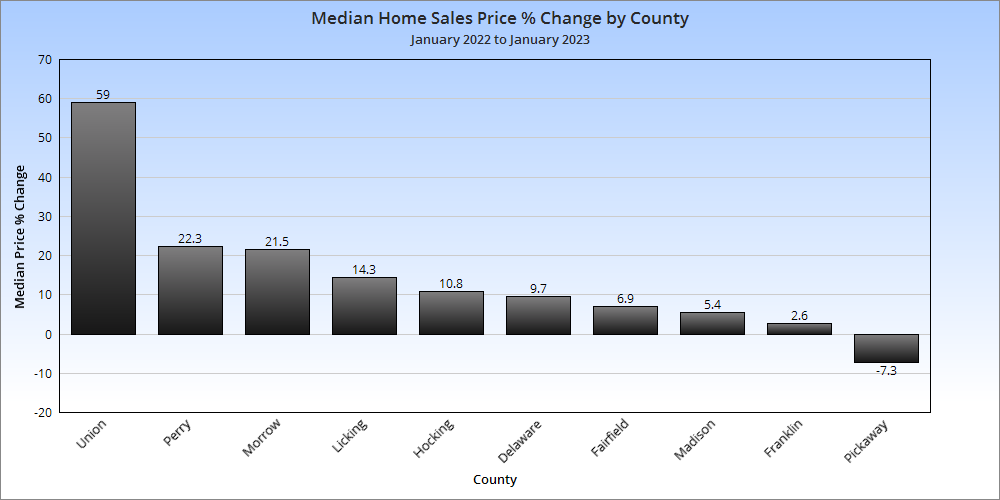

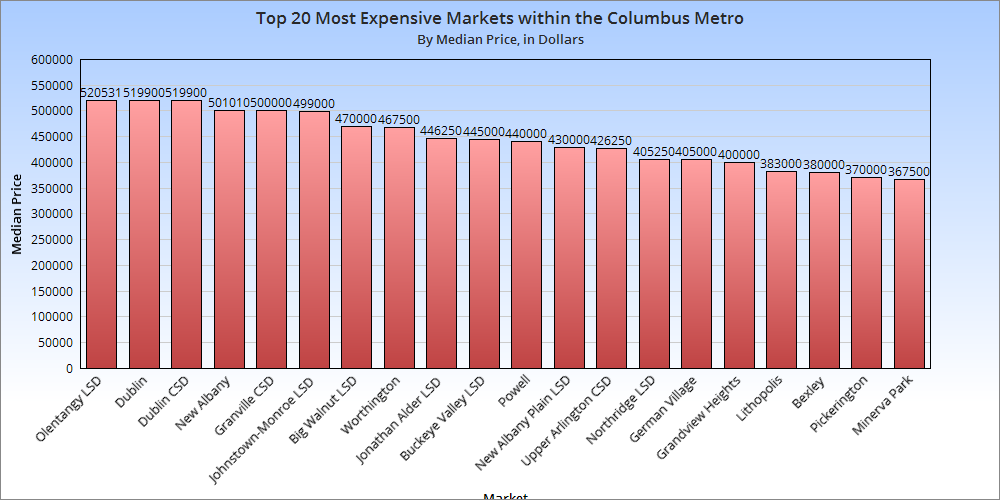

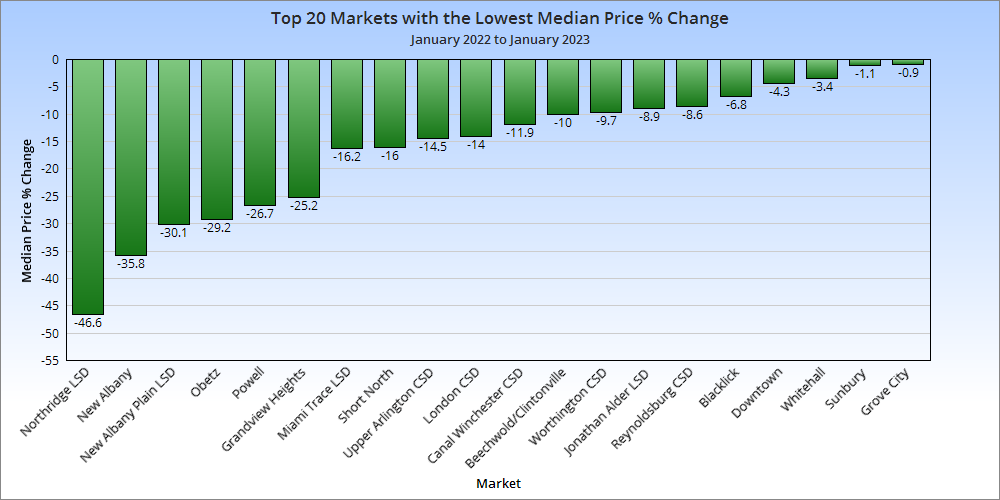

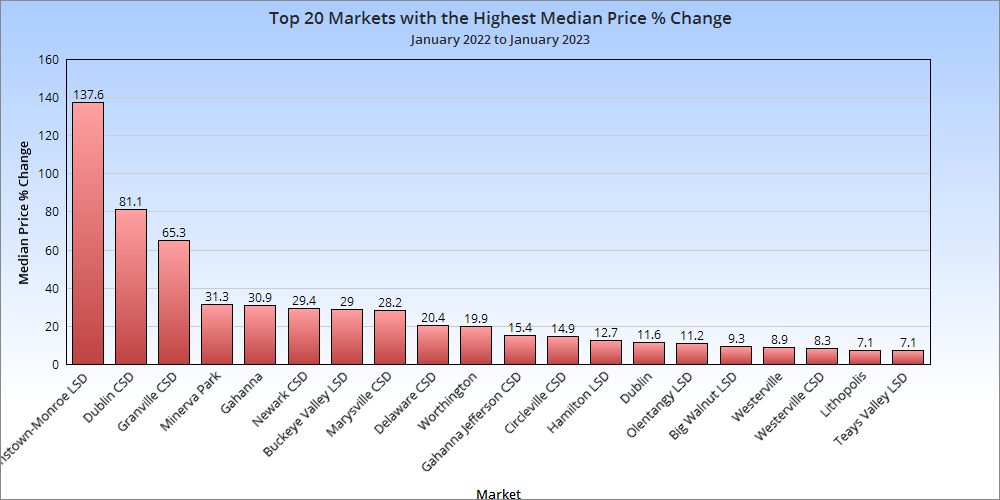

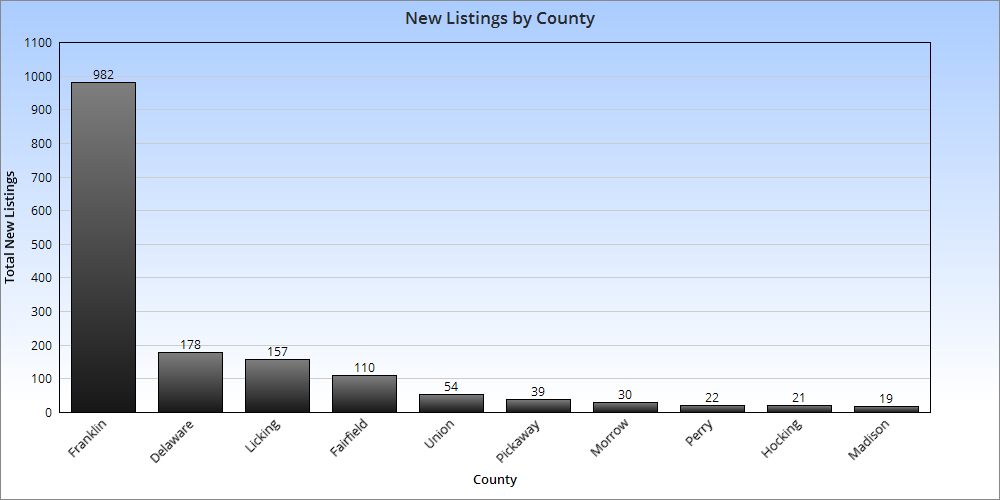

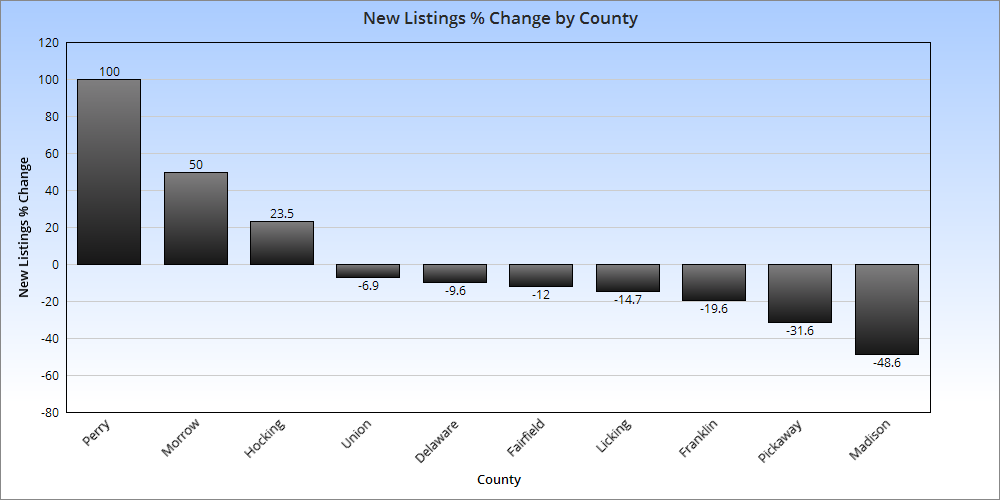

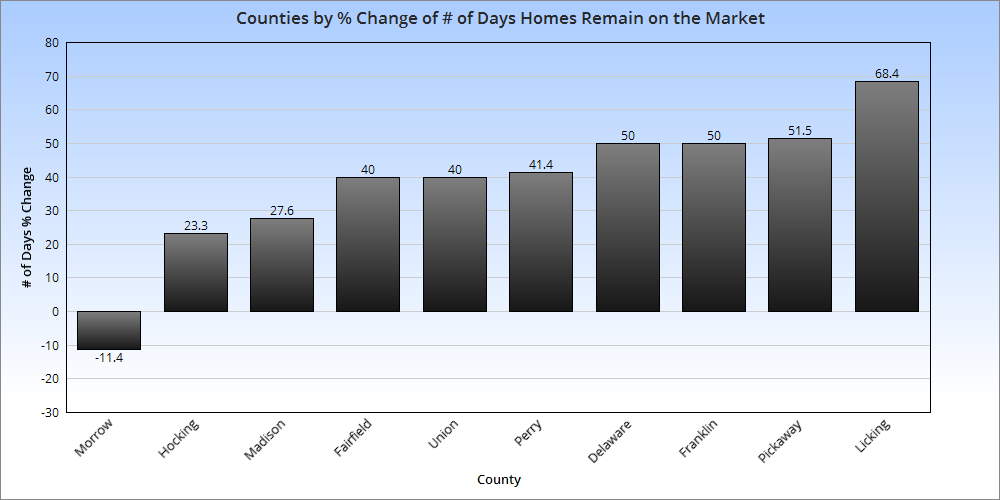

Closed sales are those sales that were completed during the month. 7 of the 10 metro counties saw declines in January Only 9 of more than 40 local markets were up year-over-year. Not sure what was going on in Union County in January, but it was well above all other counties for the month. The market overall continued to be up on price year-over-year, except in Pickaway County. Overall Market Median Sales Price in January 2023: $307,289 Based on the 10 Columbus Metro Area counties, the metro price saw a more than $39,000 increase over January, 2022. Overall Market Median Sales Price % Change in January, 2023 vs. January, 2022: +14.6% Continuing home sale declines had relatively little impact on home prices overall, which saw a strong increase over the year. It seems the Intel project’s impact may finally be making an appearance in housing numbers, with the Johnstown district seeing a huge increase in median home prices versus January 2022, 2 months before the project became official. That said, New Albany had one of the areas largest declines, but that could be due to it generally being one of the most expensive markets last year. New listings across most of the metro area were down, accounting for most of the median price increase as demand remains strong in the region. Most of the decrease came from Franklin County. Total Metro New Listings in January, 2023: 1,612 Total Metro New Listings Change from January, 2022 to January, 2023: -316 Average # of Days Homes Remain on the Market Before Sale for the Metro Overall in January, 2023: 34.0 # of Days Homes Remain on the Market Before Sale for the Metro January, 2022 to January, 2023: +8.8 Homes continued to sell more slowly than they did a year ago, now more than a week more slowly on average.

The Housing Market Update September 2022 data from Columbus Realtors continued to support that the local housing shortage is as bad as ever, with low supplies and rising prices.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

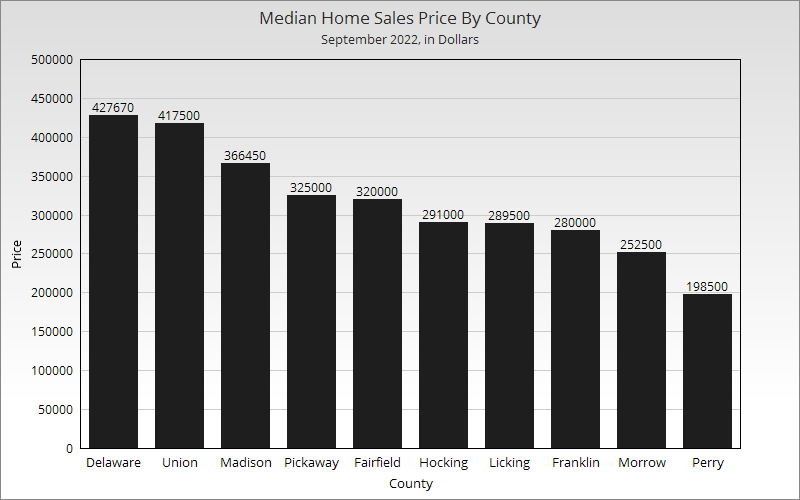

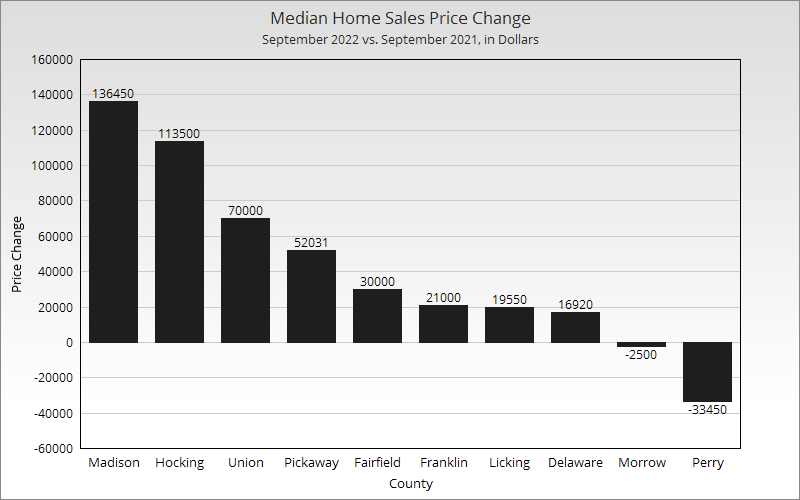

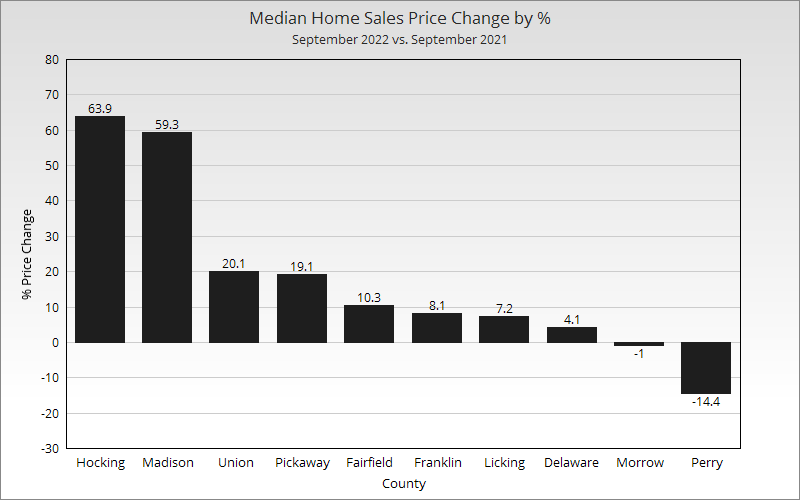

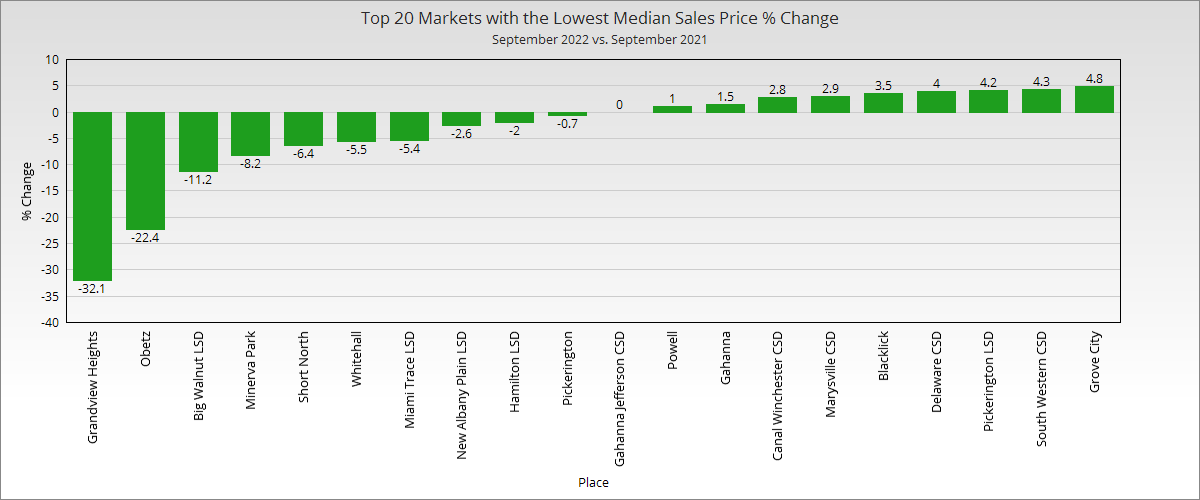

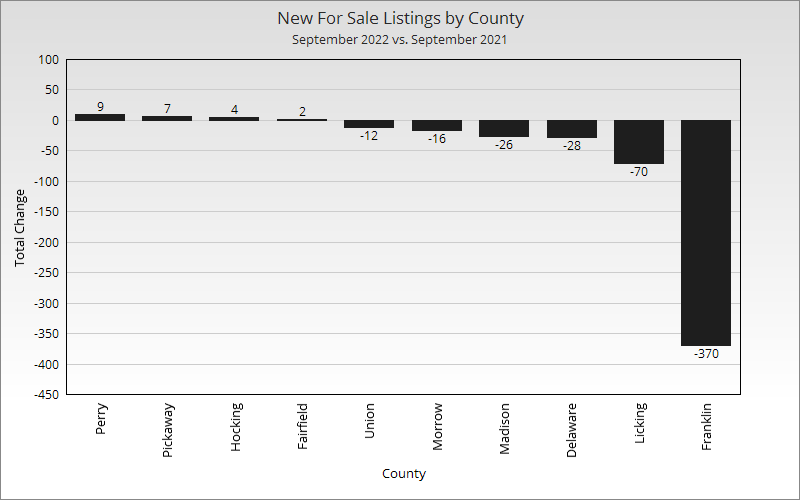

The least populated counties saw some of the largest swings either positively or negatively, which is typically the case given that prices can be determined by a much smaller number of home sales.

Overall Market Median Sales Price in September 2022: $316,812 Based on the 10 Columbus Metro Area counties, the metro price saw about a $10,000 increase over August 2022 and a more than $42,000 increase versus September 2021. Overall Market Median Sales Price % Change in September 2022 versus September 2021: +15.4%

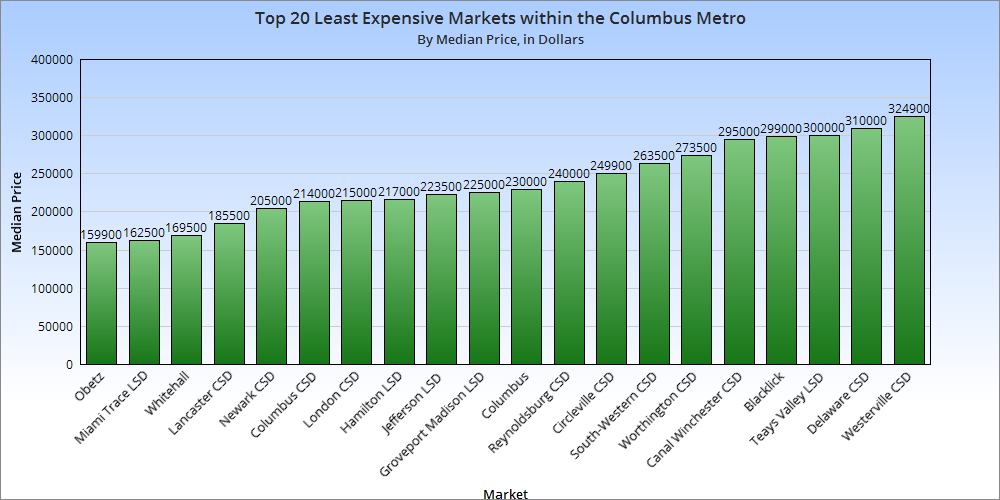

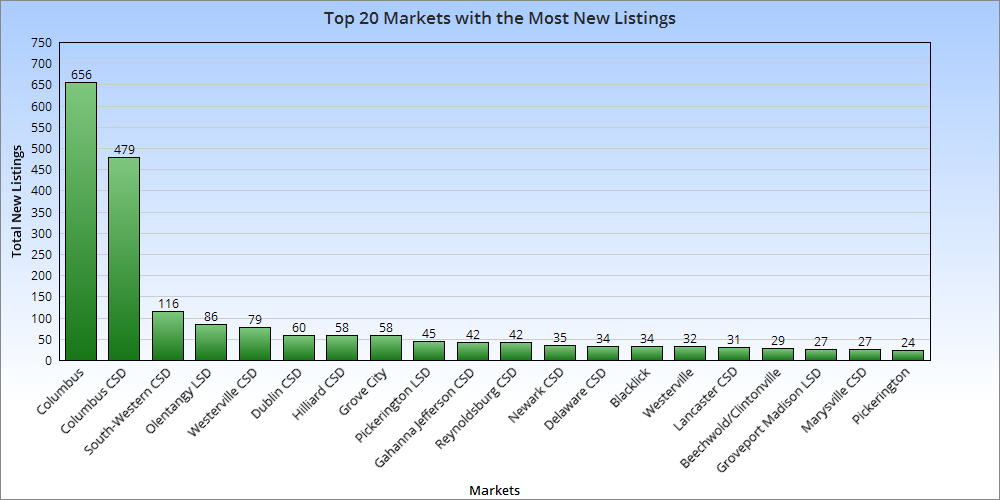

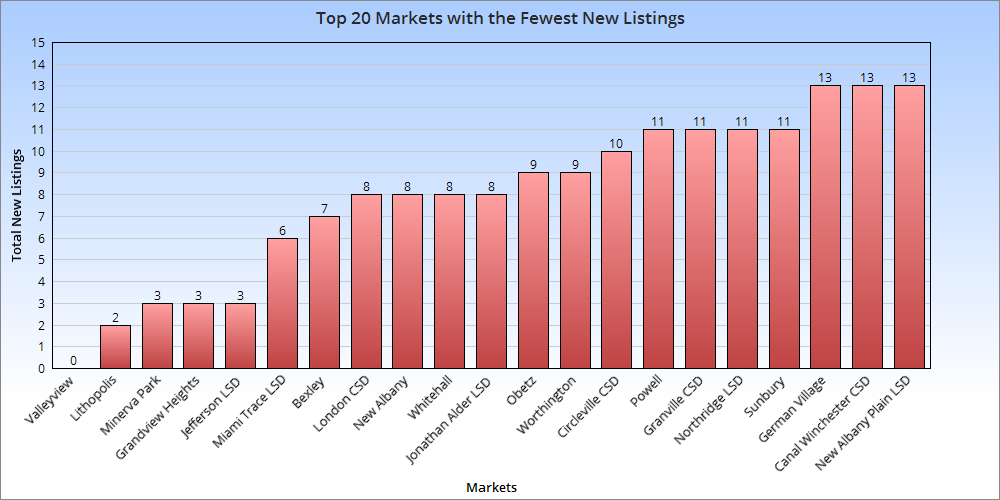

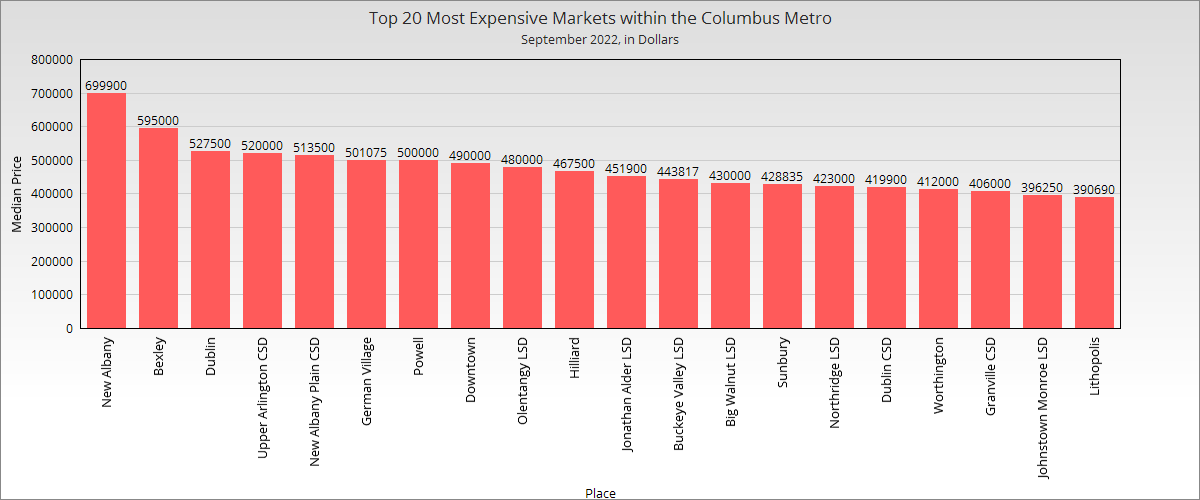

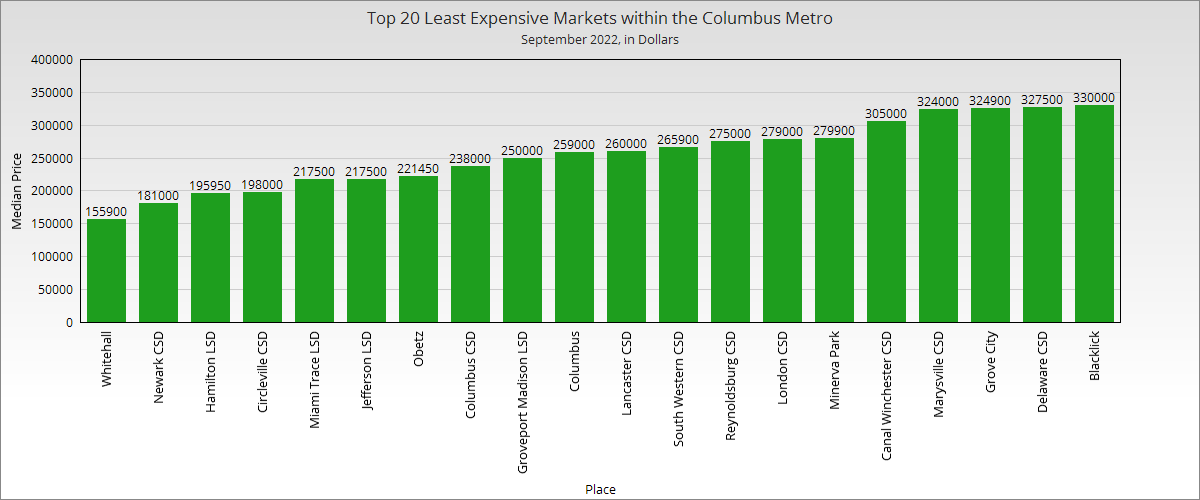

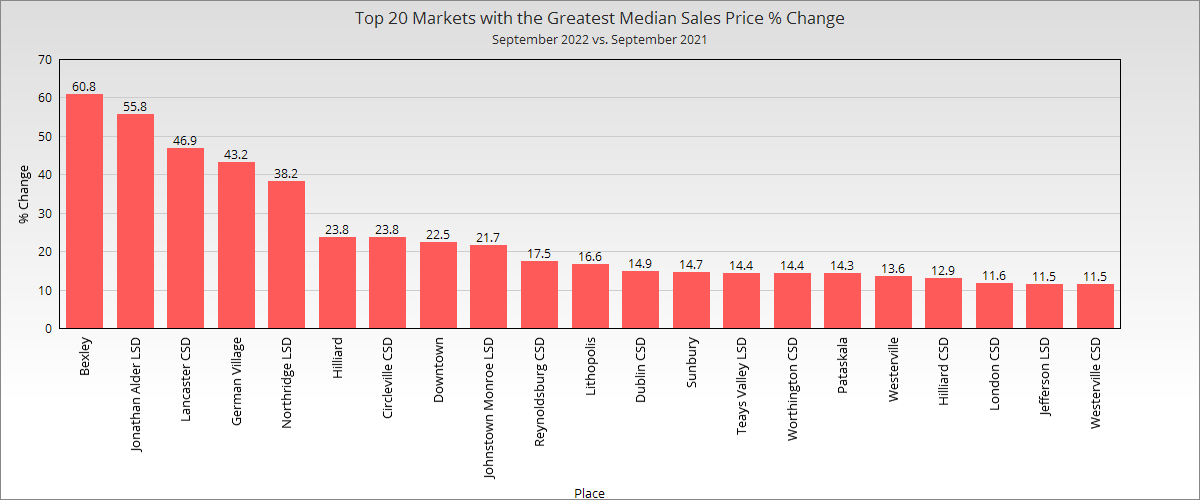

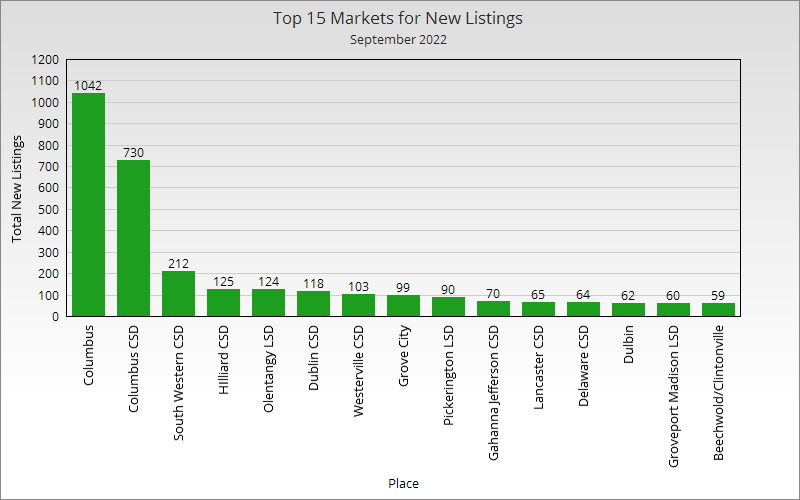

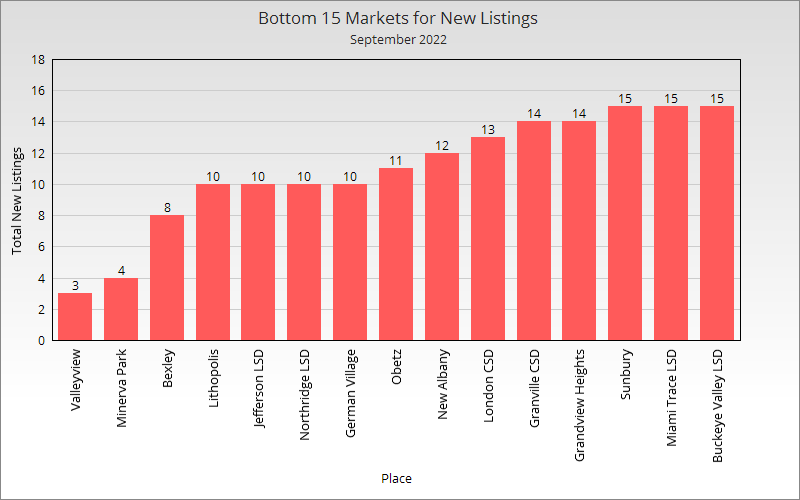

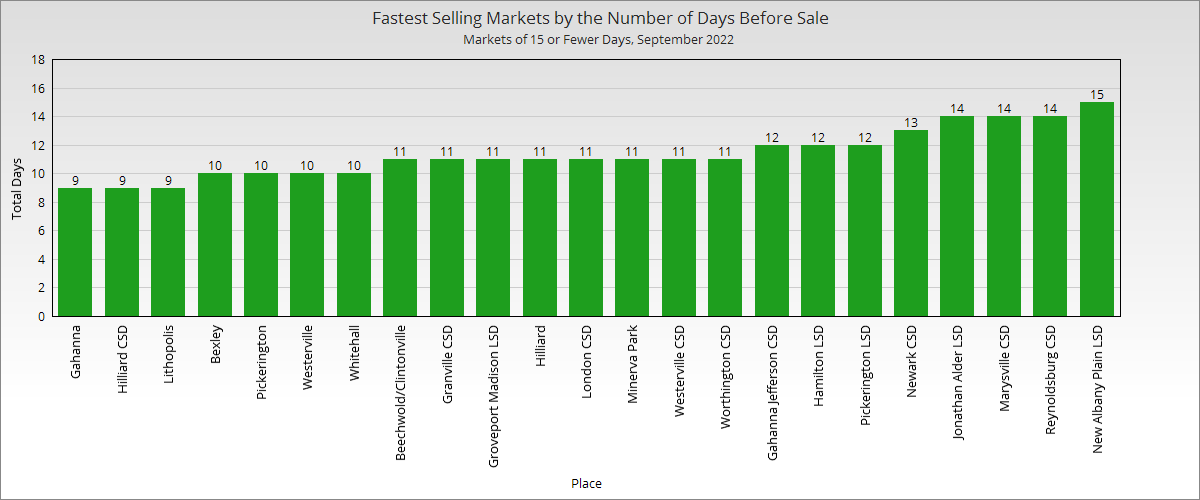

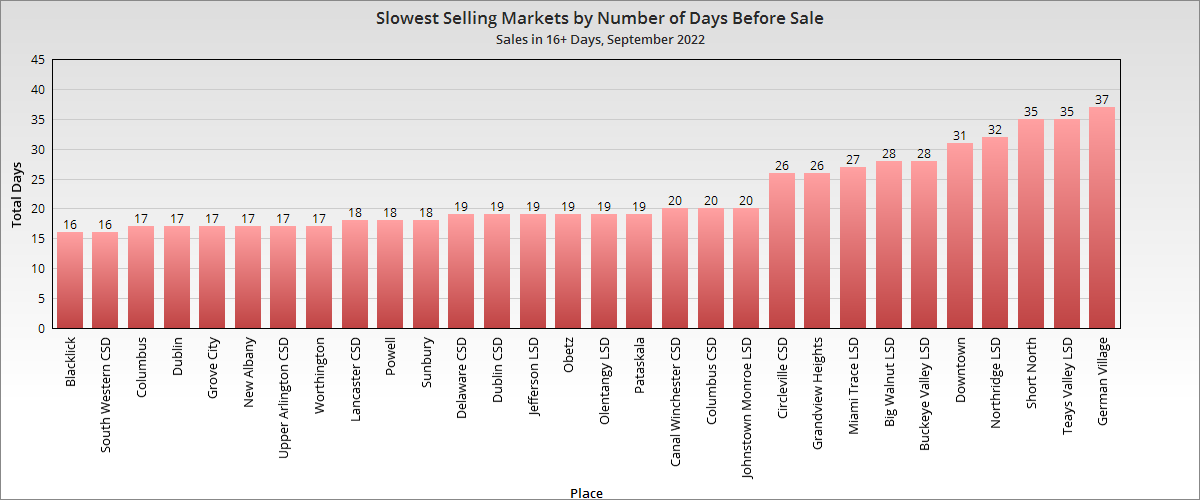

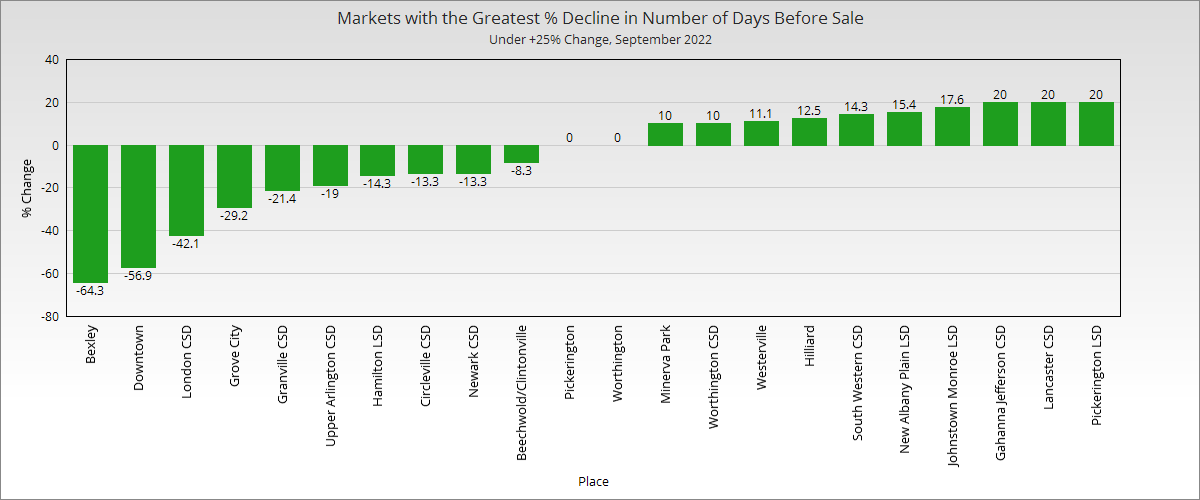

Now let’s take a look at individual neighborhoods and places within the metro area.

New Albany and some of the other expected suburbs continued to top the charts, but with prices not quite as high as over the summer.

Just 4 local markets out of more than 50 remained below the $200K market in September. Columbus itself was in it usual spot closer to the *relatively* more affordable bottom.

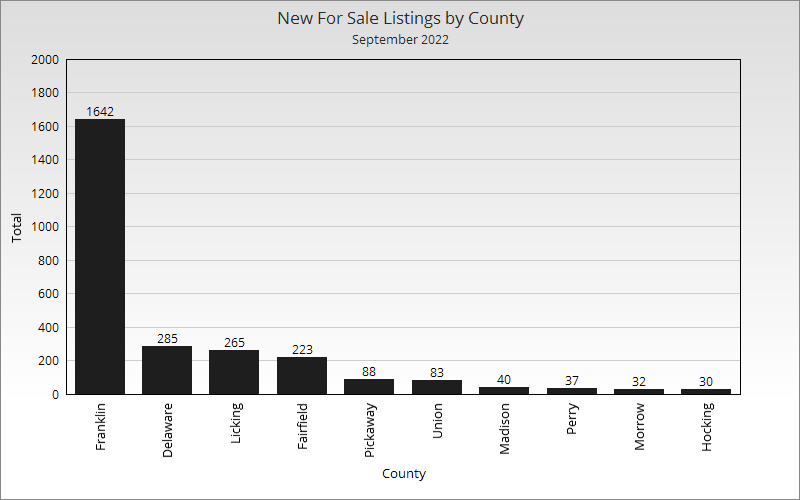

Total Metro New Listings in September 2022: 2,725 Total Metro New Listings Change from September 2021 to September 2022: -500 Year-over-year, new listings were down significantly across the metro area, but especially in Franklin County.

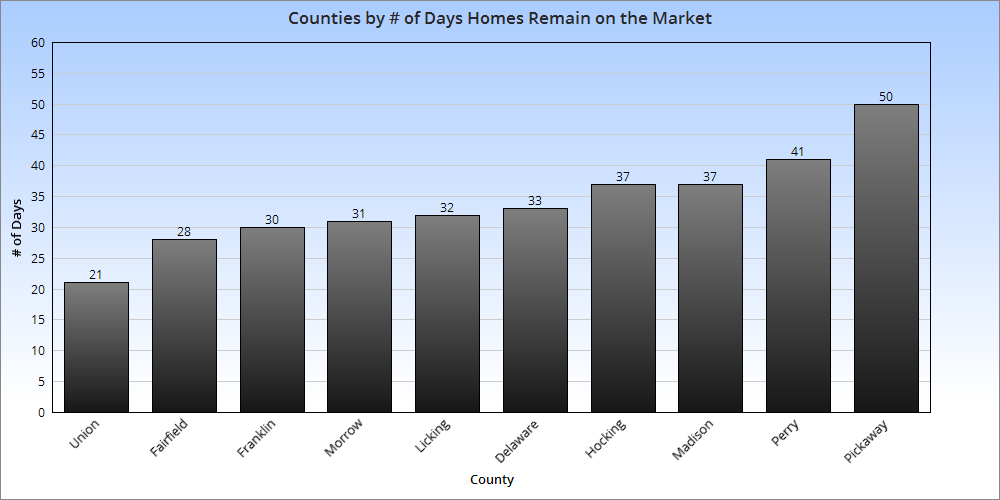

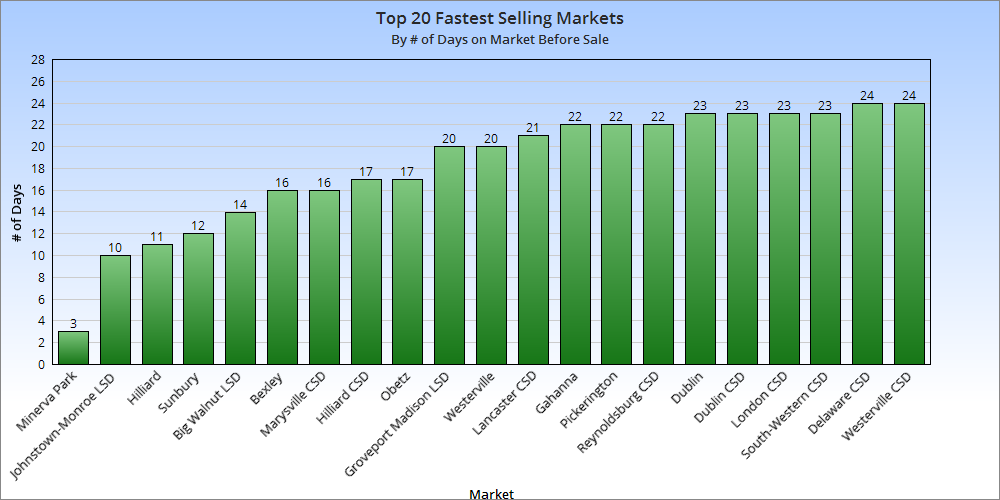

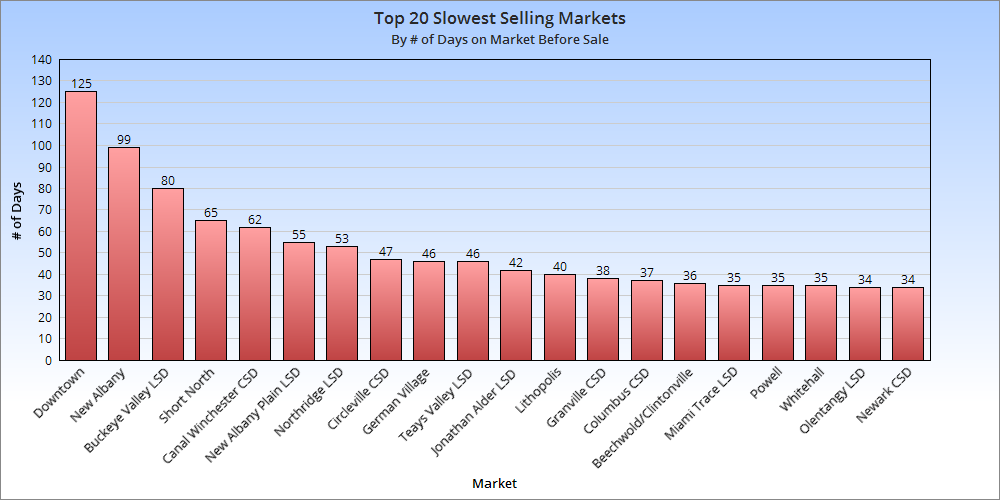

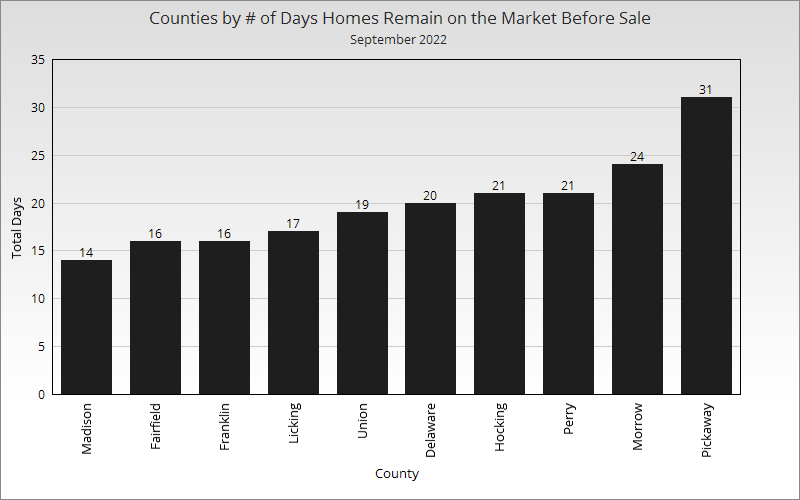

Average # of Days Homes Remain on the Market Before Sale for the Metro Overall in September 2022: 19.9 # of Days Homes Remain on the Market Before Sale for the Metro September 2021 vs. September 2022: -0.3 Homes across the market sold slightly faster than a year ago, but largely due to significant drops in a few rural counties. Most counties saw small increases.

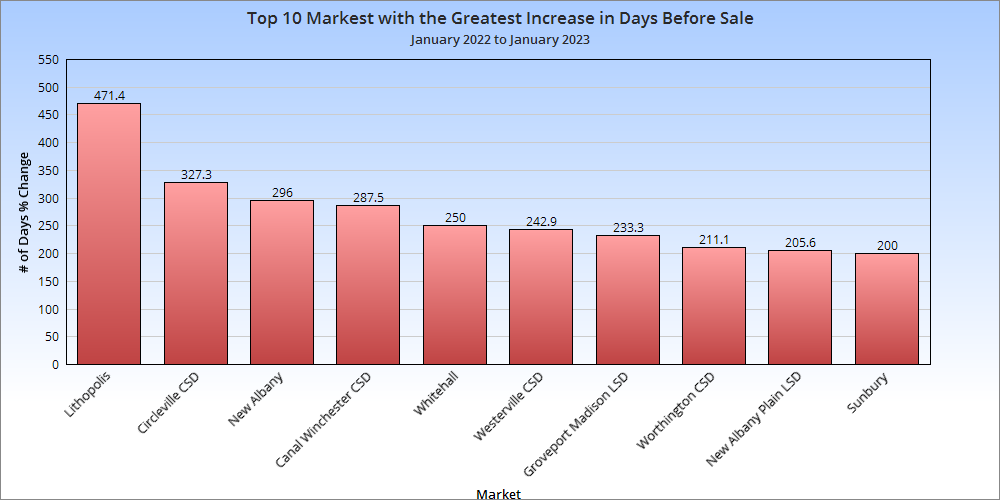

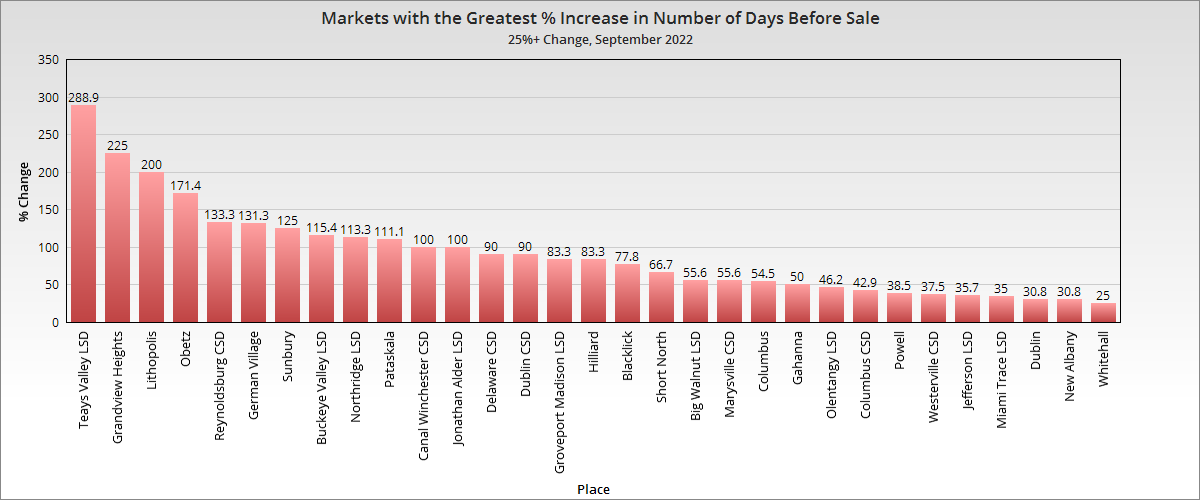

The vast majority of local markets saw substantial increases in the number of days before sale, which is pretty much the only measurement indicating the seller’s market may finally be showing some signs of weakness.

All data for the Housing Market Update comes from Columbus Realtors.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

Top 15 Most Expensive Locations By Median Sales Price in April 2022 1. New Albany: $650,000 2. New Albany Plain LSD: $635,000 3. Powell: $605,663 4. Grandview Heights: $585,000 5. Upper Arlington CSD: $580,000 6. Granville CSD: $566,500 7. German Village: $565,000 8. Bexley: $562,000 9. Dublin: $547,500 10. Olentangy LSD: $508,900 11. Worthington: $507,500 12. Dublin CSD: $480,000 13. Big Walnut LSD: $463,178 14. Hilliard: $450,000 15. Sunbury: $427,500

Top 15 Least Expensive Locations by Median Sales Price in April 2022 1. Newark CSD: $175,000 2. Whitehall: $190,000 3. Lancaster CSD: $190,000 4. Circleville CSD: $200,000 5. Miami Trace LSD: $210,000 6. Hamilton LSD: $214,500 7. Obetz: $220,000 8. London CSD: $244,750 9. Columbus CSD: $247,000 10. Groveport Madison LSD: $253,500 11. Columbus: $263,000 12. South Western CSD: $275,000 13. Jefferson LSD: $285,000 14. Reynoldsburg CSD: $299,850 15. Gahanna: $310,000 Even the cheapest markets are mostly above $200K now.

Overall Market Median Sales Price in April: $300,875 Based on the 10 Columbus Metro Area counties. This price was slightly lower than in May.

Top 15 Locations with the Highest Median Sales Price % Growth Between April 2021 and April 2022 1. Minerva Park: +59.6% 2. Lithoplis: +44.1% 3. Jefferson LSD: +43.9% 4. Miami Trace LSD: +40.0% 5. Pataskala: +39.6% 6. Granville CSD: +38.2% 7. Sunbury: +37.7% 8. Canal Winchester CSD: +36.7% 9. New Albany Plain LSD: +35.3% 10. Grove City: +30.4% 11. Groveport Madison LSD: +29.3% 12. Worthington CSD: +27.8% 13. Reynoldsburg CSD: +26.0% 14. Newark CSD: +25.0% 15. Upper Arlington CSD: +24.7%

Top 15 Locations with the Lowest Median Sales Price % Growth Between April 2021 and April 2022 1. Jonathan Alder LSD: -21.6% 2. Short North: -18.6% 3. Buckeye Valley LSD: -17.6% 4. Lancaster CSD: -5.0% 5. New Albany: -4.1% 6. Obetz: -2.3% 7. German Village: -0.9% 8. Beechwold/Clintonville: +4.3% 9. Dublin: +6.5% 10. Bexley: +6.5% 11. Dublin CSD: +9.8% 12. Hamilton LSD: +9.9% 13. Westerville: +11.9% 14. Columbus CSD: +13.8% 15. Olentangy LSD: +14.0% 16. Columbus: +15.1% Columbus core neighborhoods and Columbus overall saw some of the smallest or even negative price changes.

Overall Market Median Sales Price % Change April 2022 vs. April 2021:+19.8%

Top 10 Locations with the Most New Listings in April 2022 1. Columbus: 1,260 2. Columbus CSD: 856 3. South Western CSD: 223 4. Olentangy LSD: 170 5. Westerville CSD: 161 6. Hilliard CSD: 136 7. Dublin CSD: 131 8. Pickerington LSD: 99 9. Grove City: 93 10. Worthington CSD: 91

Top 10 Locations with the Fewest New Listings in April 2022 1. Valleyview: 1 2. Lithopolis: 3 3. Jefferson LSD: 5 4. Minerva Park: 6 5. Grandview Heights: 7 6. Northridge LSD: 8 7. Obetz: 10 8. German Village: 10 9. Sunbury: 11 10. Jonathan Alder LSD: 12 11. Hamilton LSD: 15 12. Granville CSD: 15

Total New Listings in the Columbus Metro in April 2022:+3,194 Overall Metro New Listings % Change April 2022 vs April 2021:-1.7%

Top 10 Fastest-Selling Locations by # of Days Homes Remain on the Market Before Sale in April 2022 1. Gahanna: 3 2. Jefferson LSD: 3 3. Minerva Park: 3 4. Worthington: 3 5. Blacklick: 4 6. Canal Winchester CSD: 4 7. Gahanna Jefferson CSD: 4 8. Jonathan Alder LSD: 4 9. Obetz: 4 10. Big Walnut LSD: 5 11. Hilliard CSD: 5 12. Powell: 5 13. Sunbury: 5 14. Dublin: 6 15. Hilliard: 6 16. Lithopolis: 6 17. Reynoldsburg CSD: 6 18. Whitehall: 6 19. Worthington CSD: 6 20. Hamilton LSD: 7 21. Miami Trace LSD: 7 22. Westerville: 7 23. Dublin CSD: 8 24. Groveport Madison LSD: 8 25. Upper Arlington CSD: 8 26. Beechwold/Clintonville: 9 27. Westerville CSD: 9 28. Granville CSD: 10 29. Marysville CSD: 10 30. Pickerington LSD: 10 31. Bexley: 11 32. Columbus: 11 33. Delaware CSD: 11 34. German Village: 11 35. Johnstown-Monroe LSD: 11 36. Lancaster CSD: 11 37. Newark CSD: 11 38. Olentangy LSD: 11 39. Pickerington: 11 40. Circleville CSD: 13 41. Grandview Heights: 13

Top 10 Slowest-Selling Locations by # of Days Homes Remain on the Market Before Sale in April 2022 1. Northridge LSD: 58 2. Downtown: 40 3. Short North: 31 4. London CSD: 24 5. Buckeye Valley LSD: 23 6. Grove City: 22 7. Pataskala: 21 8. New Albany: 20 9. Teays Valley LSD: 15 10. Columbus CSD: 14 11. New Albany Plain LSD: 14 12. South Western CSD: 14

Top 10 Locations with the Greatest % Decline of # of Days on the Market Before Sale April 2022 vs. April 2021 1. Miami Trace LSD: -86.3% 2. Gahanna: -76.9% 3. Gahanna Jefferson CSD: -75.0% 4. Granville CSD: -74.4% 5. Blacklick: -71.4% 6. German Village: -71.1% 7. New Albany Plain LSD: -64.1% 8. Obetz: -63.6% 9. New Albany: -59.2% 10. Upper Arlington CSD: -55.6%

Top 10 Locations with the Lowest % Decline of # of Days on the Market Before Sale April 2022 vs. April 2021 1. Lithopolis: +200.0% 2. Northridge LSD: +176.2% 3. Grove City: +69.2% 4. Sunbury: +66.75 5. Pataskala: +61.5% 6. London CSD: +60.0% 7. South Western CSD: +55.6% 8. Downtown: +48.1% 9. Westerville: +40.0% 10. Delaware CSD: +37.5% 11. Johnstown-Monroe LSD: +37.5%

Total # of Days Homes Remain on the Market Before Sale Across the Metro Overall: 13.7 Overall Metro Days on Market % Change April 2022 vs April 2021: -35.7% Homes were selling on average almost 8 days after than a year ago.

Around Columbus and Franklin County, tax incentives and abatements are granted to properties either for new development or to encourage improvements to existing buildings. Most of these incentives are given to properties in urban neighborhoods that have suffered from a lack of investment. However, in recent years, studies have shown that the distribution of them is both uneven and highly controversial, often going to rich developers in already well-established neighborhoods rather than those that need them the most. The link of the Columbus property tax abatement map provides both descriptions of the types of tax incentives used locally, as well as a map that shows what properties get what incentives and how much they amount to.

In addition to abatements and incentives, TIFs, or Tax Increment Financing, uses targeted tax collection in specific areas to make improvements within said districts. Unlike tax abatements/incentives, TIFs can be found almost anywhere, and are regularly used in both suburban and urban neighborhoods, and are not always tied to improving declined areas.

The local housing market update May 2021 is finally out, and the trends continue to show a strong sellers market. Prices continued to accelerate upward and supply continued to lag way behind, pushing home sales to occur even faster than they have been in recent months.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

Top 15 Most Expensive Locations By Median Sales Price in May 2021 1. New Albany: $810,000 2. German Village: $630,000 3. New Albany Plain LSD: $570,000 4. Dublin: $528,750 5. Bexley: $497,500 6. Upper Arlington CSD: $495,000 7. Worthington: $461,420 8. Powell: $460,000 9. Dublin CSD: $450,000 10. Olentangy LSD: $445,000 11. Buckeye Valley LSD: $406,790 12. Granville CSD: $402,500 13. Short North: $400,450 14. Grandview Heights: $394,000 15. Jonathan Alder LSD: $390,000

New Albany proper posted an astronomical median price in May, reaching unprecedented numbers for a Columbus suburb.

Top 15 Least Expensive Locations by Median Sales Price in May 2021 1. Whitehall: $138,000 2. Valleyview: $157,500 3. Groveport Madison LSD: $175,825 4. Lancaster CSD: $176,000 5. Circleville CSD: $182,000 6. Newark CSD: $184,250 7. Jefferson LSD: $207,500 8. Columbus CSD: $220,000 9. London CSD: $225,000 10. Hamilton LSD: $237,000 11. Columbus: $240,000 12. Reynoldsburg CSD: $245,500 13. South-Western CSD: $249,900 14. Canal Winchester CSD: $260,000 15. Teays Valley LSD: $268,894

In general, the further out the place from Columbus, the cheaper the location, but there are some exceptions. Whitehall and Columbus proper remain relatively affordable compared to most locations in the metro.

Overall Market Median Sales Price in May 2021: $227,088 The overall market is defined by Columbus Metro Area counties.

Top 15 Locations with the Highest Median Sales Price % Growth Between May 2020 and May 2021 1. German Village: +59.5% 2. Worthington: +54.6% 3. Obetz: +52.2% 4. New Albany Plain LSD: +40.7% 5. Hamilton LSD: +39.4% 6. Dublin CSD: +32.0% 7. Delaware CSD: +32.0% 8. Dublin: +31.4% 9. Pickerington: +30.3% 10. New Albany: +29.7% 11. Newark CSD: +29.4% 12. Worthington CSD: +29.1% 13. Westerville CSd: +28.6% 14. Pataskala: +27.0% 15. Jonathan Alder LSD: +25.8%

Top 15 Locations with the Lowest Median Sales Price % Growth Between May 2020 and May 2021 1. Lancaster CSD: -7.3% 2. Jefferson LSD: -5.5% 3. Downtown Columbus: -4.2% 4. Hilliard: -0.5% 5. Teays Valley LSD: +3.5% 6. Powell: +5.1% 7. Big Walnut LSD: +6.2% 8. Grandview Heights: +6.8% 9. Granville CSD: +7.6% 10. Short North: +7.6% 11. Canal Winchester CSD: +8.3% 12. Minerva Park: +8.4% 13. London CSD: +10.3% 14. Circleville CSD: +11.3% 15. Buckeye Valley LSD: +11.4%

There were fewer locations down year-over-year in May than in previous months, though urban areas generally saw lower increases.

Overall Market Median Sales Price % Change May 2021 vs. May 2020: +18.6%

Top 10 Locations with the Most New Listings in May 2021 1. Columbus: 1,467 2. Columbus CSD: 972 3. South-Western CSD: 217 4. Hilliard CSD: 171 5. Westerville CSD: 168 6. Olentangy LSD: 166 7. Dublin CSD: 166 8. Worthington CSD: 118 9. Pickerington LSD: 115 10. Upper Arlington CSD: 101

Top 10 Locations with the Fewest New Listings in May 2021 1. Valleyview: 2 2. Lithopolis: 5 3. Minerva Park: 5 4. Jefferson LSD: 6 5. Obetz: 8 6. Sunbury: 8 7. Grandview Heights: 10 8. Johnstown-Monroe LSD: 11 9. Whitehall: 12 10. Circleville CSD: 14

Urban areas and major suburbs saw increases in supply versus previous months, but because sales were also stronger, it didn’t help with actual supply or prices.

Total New Listings in the Columbus Metro in May 2021: +3,468 Overall Metro New Listings % Change May 2021 vs May 2020: +14.3%

Top 10 Fastest-Selling Locations by # of Days Homes Remain on the Market Before Sale in May 2021 1. Jonathan Alder LSD: 3 2. Valleyview: 3 3. Canal Winchester CSD: 4 4. Groveport Madison LSD: 4 5. Lithopolis: 4 6. German Village: 5 7. Worthington: 5 8. Worthington CSD: 5 9. Beechwold/Clintonville: 6 10. Blacklick: 6 11. Gahanna: 6 12. Marysville CSD: 6 13. Pickerington LSD: 6 14. Powell: 6 15. Westerville CSD: 6 16. Whitehall: 6

Top 10 Slowest-Selling Locations by # of Days Homes Remain on the Market Before Sale in May 2021 1. Short North: 51 2. Downtown Columbus: 39 3. Johnstown-Monroe LSD: 28 4. Bexley: 25 5. Lancaster CSD: 25 6. Jefferson LSD: 23 7. Obetz: 22 8. Buckeye Valley LSD: 21 9. Dublin: 19 10. Olentangy LSD: 18

Top 10 Locations with the Greatest % Decline of # of Days on the Market Before Sale May 2021 vs May 2020 1. Powell: -91.2% 2. Jonathan Alder LSD: -90.6% 3. Minerva Park: -85.7% 4. Circleville CSD: -84.2% 5. Whitehall: -82.9% 6. London CSD: -80.0% 7. Sunbury: -78.9% 8. Newark CSD: -78.0% 9. Upper Arlington CSD: -76.5% 10. Granville CSD: -75.8%

Top 10 Locations with the Lowest % Decline of # of Days on the Market Before Sale May 2021 vs May 2020 1. Short North: +264.3% 2. Valleyview: +50.0% 3. Bexley: +13.6% 4. Downtown Columbus: +11.4% 5. Lancaster CSD: -3.8% 6. Teays Valley LSD: -11.1% 7. Dublin: -26.9% 8. Reynoldsburg CSD: -29.4% 9. Westerville: -33.3% 10. Pataskala: -38.5%

% Change for the # of Days Homes Remain on the Market Before Sale Across the Metro Overall: 14

The market’s sales pace only increased further in May, with the entire metro’s supply of homes selling in an average of just 2 weeks. Many locations were selling at far faster rates, however.

A handy link is the Columbus Realtors website, which most of this data is derived from.