A little more than 4 years ago, I posted numbers on the recovery of Ohio downtowns, and what that might mean for the future. That post has proven to be one of the site’s most popular. I figured it was time to take a look at their continuing changes.

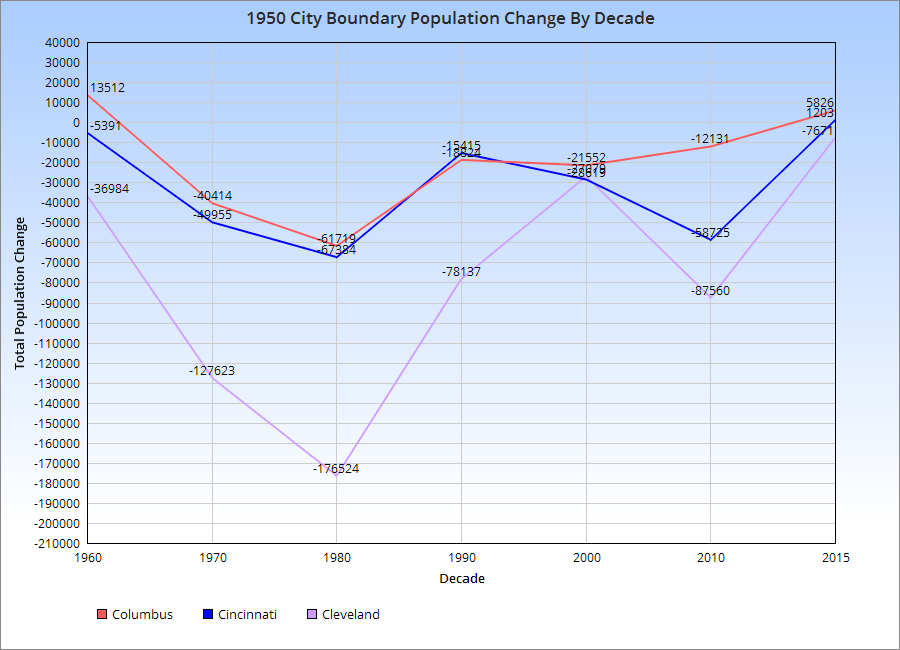

You can see by the chart for the 1950 Boundary population, the urban core of each city, that all 3-Cs suffered population losses post-1950. However, the rate of losses gradually declined, and 2 of the cities, Columbus and Cincinnati, appear to be growing in this boundary since at least 2010. Cleveland continues to lose.

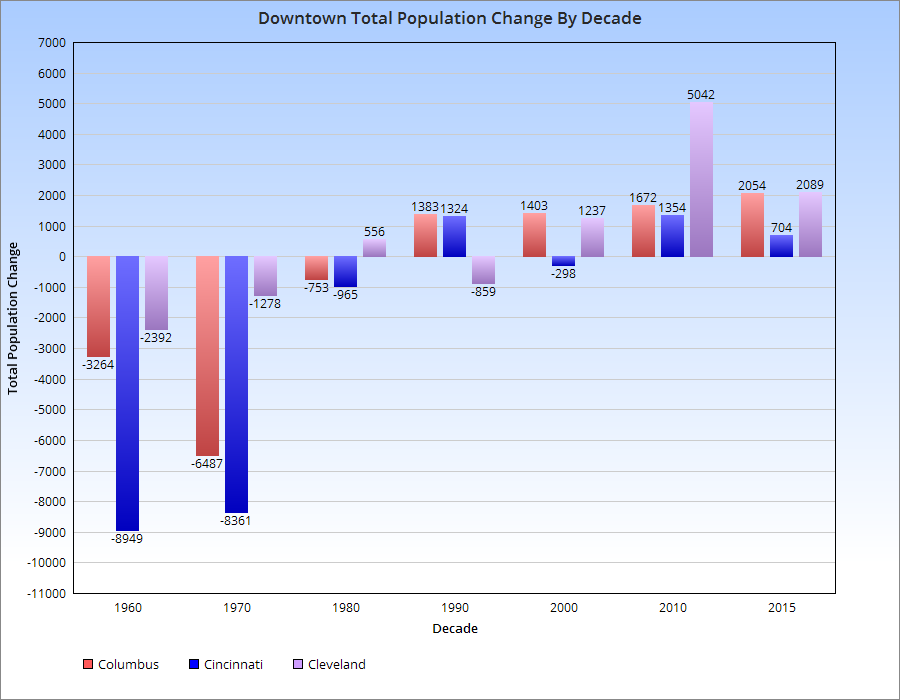

This is shown further by the chart below.

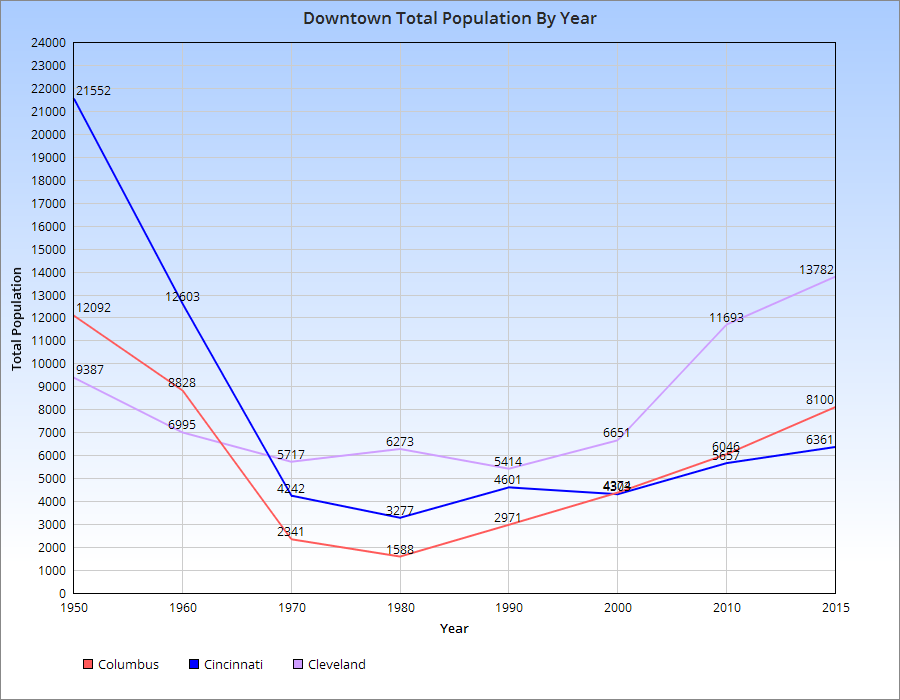

As far as the actual Downtowns of each, here are the population trends.

For the most part, population declines in the 3-Cs peaked around 1980, give or take a decade. Since then, all of them have seen increases, with Cleveland seeing the most rapid increase and Cincinnati the least. Columbus has seen steady, but increasingly rapid growth with each subsequent decade since 1980.

The recent housing market update January 2017 edition information comes from Columbus Realtors.

Note: LSD= Local School District, CSD= City School District. In both cases, school district boundaries differ from city boundaries.

Top 15 Most Expensive Locations By Median Sales Price in January 2017 1. New Albany: $535,000 2. New Albany Plain LSD: $397,450 3. German Village: $376,000 4. Powell: $354,950 5. Dublin: $343,600 6. Granville CSD: $330,000 7. Bexley: $325,000 8. Upper Arlington CSD: $319,500 9. Olentangy LSD: $315,000 10. Big Walnut LSD: $306,250 11. Dublin CSD: $271,500 12. Worthington: $270,000 13. Buckeye Valley LSD: $259,000 14. Sunbury: $253,000 15. Downtown: $243,750

Top 15 Least Expensive Locations by Median Sales Price in January 2017 1. Obetz: $80,100 2. Hamilton LSD: $80,100 3. Whitehall: $85,950 4. Newark CSD: $86,900 5. Lancaster CSD: $103,000 6. Jefferson LSD: $123,000 7. London CSD: $124,000 8. Groveport Madison LSD: $125,900 9. Reynoldsburg CSD: $125,950 10. Columbus CSD: $129,900 11. South-Western CSD: $131,000 12. Columbus: $140,026 13. Jonathan Alder LSD: $150,000 14. Minerva Park: $159,500 15. Grove City: $160,950

Overall Market Median Sales Price in January 2017: $160,368 Median Sales Price Change January 2016-January 2016: +$3,172

Top 15 Locations with the Highest Median Sales Price % Growth Between January 2016 and January 2017 1. Whitehall: +69.5% 2. Circleville CSD: +64.9% 3. Sunbury: +63.0% 4. Jefferson LSD: +53.5% 5. Big Walnut LSD: +44.1% 6. Canal Winchester CSD: +40.9% 7. Westerville: +29.8% 8. Westerville CSD: +27.3% 9. Powell: +25.4% 10. Pataskala: +24.0% 11. Olentangy LSD: +23.5% 12. Gahanna Jefferson CSD: +21.8% 13. Grandview Heights: +21.2% 14. Granville CSD: +20.0% 15. Pickerington: +17.7%

Top 15 Locations with the Lowest Median Sales Price % Growth Between January 2016 and January 2017 1. London CSD: -53.5% 2. Obetz: -38.3% 3. Hamilton LSD: -27.1% 4. Jonathan Alder LSD: -25.2% 5. Buckeye Valley LSD: -23.0% 6. Reynoldsburg CSD: -18.7% 7. Hilliard: -17.7% 8. Lancaster CSD: -17.6% 9. Grove City: -15.3% 10. Dublin CSD: -12.8% 11. Johnstown-Monroe LSD: -10.8% 12. Upper Arlington CSD: -8.5% 13. Newark CSD: -8.1% 14. Dublin: -7.1% 15. South-Western CSD: -6.4%

Overall Market Median Sales Price % Change January 2016-January 2017: +2.0%

Top 10 Locations with the Most New Listings in January 2017 1. Columbus: 829 2. Columbus CSD: 544 3. South-Western CSD: 136 4. Olentangy LSD: 122 5. Westerville CSD: 100 6. Hilliard CSD: 94 7. Dublin CSD: 89 8. Worthington CSD: 66 9. Dublin: 64 10. Pickerington LSD: 60

Top 10 Locations with the Fewest New Listings in January 2017 1. Valleyview: 0 2. Lithopolis: 1 3. Minerva Park: 2 4. Sunbury: 2 5. Obetz: 3 6. Johnstown Monroe LSD: 5 7. Jefferson LSD: 8 8. Jonathan Alder LSD: 8 9. German Village: 8 10. Hamilton LSD: 8 11. Northridge LSD: 9

Total New Listings in the Columbus Metro in January 2017: 2,002 Overall Metro New Listings % Change January 2016-January 2017: -1.9%

Top 10 Fastest-Selling Locations by # of Days Homes Remain on the Market Before Sale in January 2017 1. Obetz: 18 2. Sunbury: 21 3. Pataskala: 22 4. Jefferson LSD: 26 5. Gahanna: 28 6. Minerva Park: 28 7. Delaware CSD: 29 8. Bexley: 31 9. Hilliard CSD: 31 10. Pickerington: 31 11. Worthington CSD: 31

Top 10 Slowest-Selling Locations by # of Days Homes Remain on the Market Before Sale in January 2017 1. Dublin: 96 2. New Albany: 93 3. Dublin CSD: 82 4. Powell: 80 5. Granville CSD: 79 6. Olentangy LSD: 78 7. Downtown: 77 8. Grandview Heights: 76 9. New Albany Plain LSD: 68 10. Canal Winchester CSD: 67 11. New Albany CSD: 65 12. Upper Arlington CSD: 62 13. Circleville CSD: 61 14. Johnstown Monroe LSD: 61 15. Hamilton LSD: 60

# of Days For-Sale Homes Remain on the Market Before Sale Across the Metro Overall: 51.6 Change in # of Days Before Sale January 2016-January 2017: -22.0

Top 10 Locations with the Greatest % Decline of # of Days on the Market Before Sale January 2016-January2017 1. Obetz: -89.2% 2. Pataskala: -64.5% 3. Whitehall: -64.3% 4. Circleville CSD: -56.1% 5. Gahanna: -53.3% 6. Grove City: -49.2% 7. Delaware CSD: -44.2% 8. Bexley: -40.4% 9. Pickerington LSD: -39.7% 10. Worthington CSD: -38.0%

Top 10 Locations with the Lowest % Decline of # of Days on the Market Before Sale January 2016-January 2017 1. German Village: +161.1% 2. Worthington: +123.8% 3. Powell: +77.8% 4. Grandview Heights: +46.2% 5. Big Walnut LSD: +41.5% 6. Minerva Park: +40.0% 7. Jonathan Alder LSD: +37.8% 8. Canal Winchester CSD: +31.4% 9. Marysville CSD: +28.3% 10. Johnstown Monroe LSD: +27.1%

% Change for the # of Days Homes Remain on the Market Before Sale Across the Metro Overall: -29.9%

The US Census recently released 2015 census tract population density data, including census tract population density. I figured midway through the decade would be a good point to update where these stand because they give greater insight in smaller-scale population changes. I looked at all the census tracts in Franklin County and came up with the following map series.

First, the population in 2015.

Next, the population density of tracts in 2010, as reference.

And now 2015.

On the surface, it’s difficult to see the changes, but put side by side, you can tell there have been a lot of increases across the county. To make this more visible, I made the following maps.

You can see that some of the strongest density increases occurred around Downtown and the Short North, New Albany, parts of the Campus area, and Dublin.

The map above gives a straightforward look at where the density increased and decreased. As you can see, the increases FAR outweighed the decreases. Most of the latter were scattered except across the Far South Side and parts of the Whitehall area.

Here were the top 20 most dense census tracts in 2015. 1. 1810: 29,508.2 South Campus/Victorian Village 2. 1121: 25,287.9 Main Campus 3. 13: 21,961.4 Campus/Indianola Terrace 4. 1110: 18168.6 North Campus/Tuttle Park 5. 10: 17386.3 Campus/SoHud 6. 12: 16,981.9 Campus/Iuka Ravine 7. 20: 13,030.5 Short North/Victorian Village 8. 17: 12,872.3 Weinland Park 9. 6: 12,153.6 Old North Columbus 10. 21: 10,853.5 Short North/High Street 11. 8163: 10,255.3 Lincoln Village/Southwest Columbus 12: 4810: 9,557.4 South Central Hilltop 13. 47: 9,492.7 North Central Hilltop 14. 6352: 9,434.0 Northwest Columbus/Henderson Road 15. 57: 9,257.4 Brewery District/South German Village 16. 5: 9,177.9 Old North Columbus 17. 6933: 9,090.9 Forest Park East 18. 16: 8,980.5 Weinland Park 19. 4620: 8,928.6 North Central Hilltop 20. 1820: 8743.3 Victorian Village

It’s obvious that the High Street corridor is the most dense of the city, racking up most of the top 20.

Now here are the 20 tracts with the largest density increases 2010-2015. 1. 1121: 4,375.9 2. 6: 2,178.5 3. 21: 1,934.9 4. 22: 1,478.1 5. 40: 1,107.7 South Downtown 6. 1820: 1,044.1 7. 20: 921.7 8. 38: 904.3 Old Towne East 9. 5: 861.2 10. 210: 833.9 Clintonville 11. 32: 751.1 Arena District West/West Victorian Village 12. 730: 736.9 13. 7551: 656.0 Somerset/South Easton 14. 7951: 610.4 West Columbus 15. 6372: 574.6 Hayden Falls/Sawmill Road 16. 7209: 514 New Albany 17. 7395: 497.6 Blacklick/East Broad 18. 10: 492.8 19. 8230: 449.3 Westland 20. 710: 447.3 West-Central Linden

And finally, the top 20 largest declines 2010-2015. 1. 13: -2,964.3 2. 12: -1,625.1 3. 42: -1,620.8 Scioto Peninsula/East Franklinton 4. 920: -902.2 Northeast Linden 5. 17: -775.4 6. 50: -554.4 Franklinton 7. 61: -485.7 South High Street 8. 59: -441.9 Near South Side/Deshler Park 9. 4620: -380.4 10. 720: -380.2 11. 4610: -335.4 12. 820: -305.4 North Linden 13. 7721: -305.2 North Linden 14. 45: -258.1 North Hilltop 15. 60: -253.2 Vassor Village 16. 810: North Central Linden 17. 7532: -240.3 Morse Road/Easton 18. 2520: -240.1 Near East Side/King-Lincoln 19. 47: -206.6 20. 9333: -194.9 Linwood

So there you have it. The Census Tract Maps page gives demographic and population data for census tracts going back to 1930.

The US Census recently released demographic information for census tracts for 2015. Here are some quick maps for Franklin County for median household income.

First, median household income for both 2010 and 2015.

And the % change between 2010-2015.

As can be seen, a lot of the greatest improvements over the 5-year period were around Downtown, the Near East Side, North High, South High and around some of the higher-income suburbs like Upper Arlington and the New Albany area.

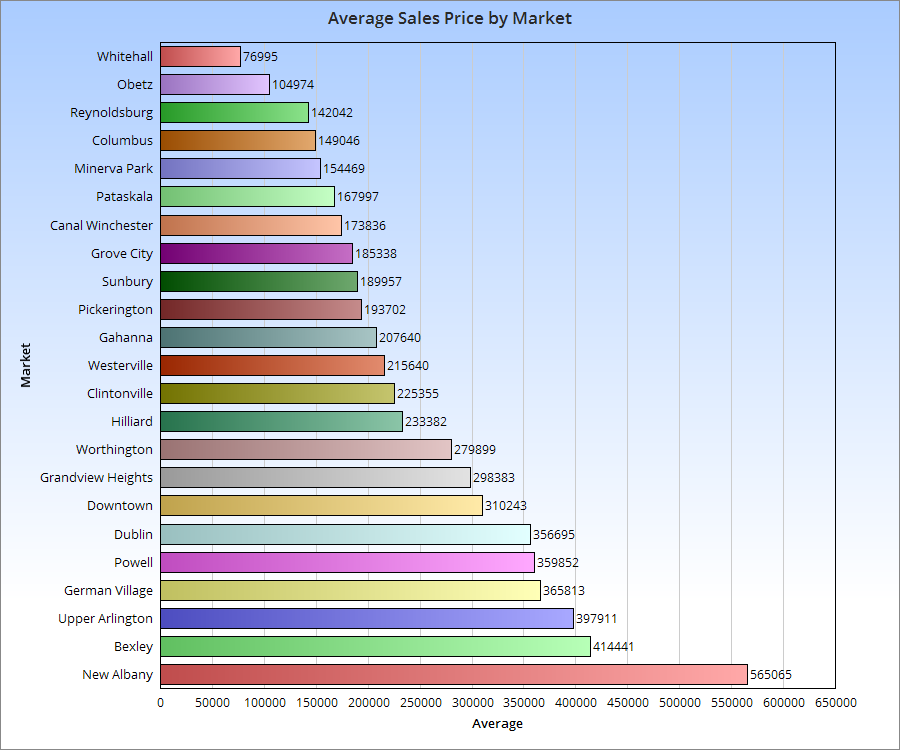

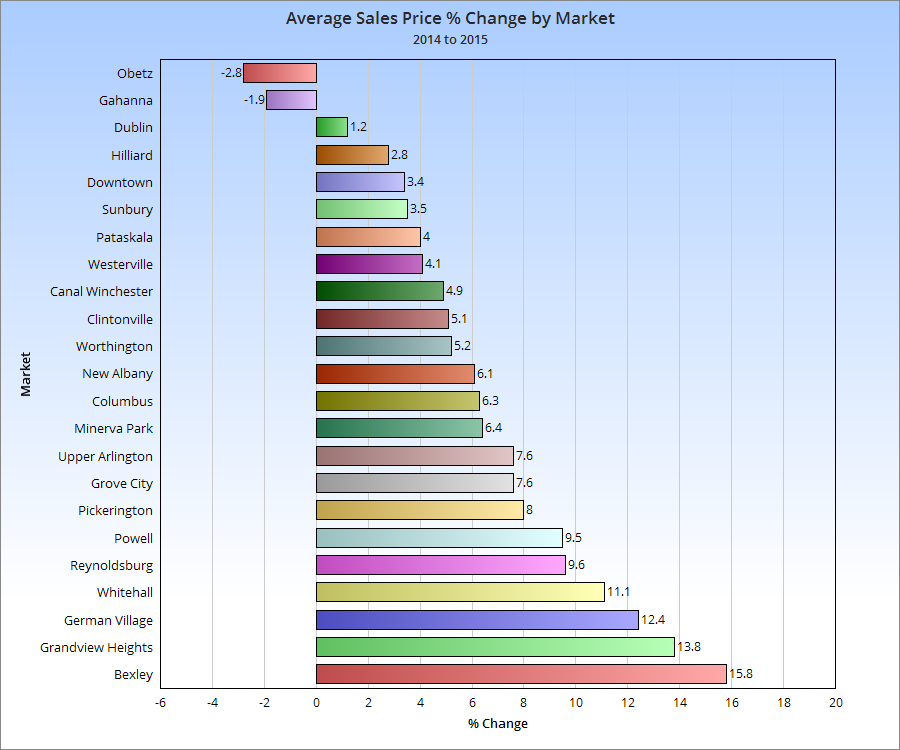

The 2015 housing market was one of the strongest since before the recession, and 2016 looks to do even better. An ongoing problem, especially within the more urban markets, is a historically low inventory of available homes for sale. This has been a problem for several years now, as construction has failed to match demand.

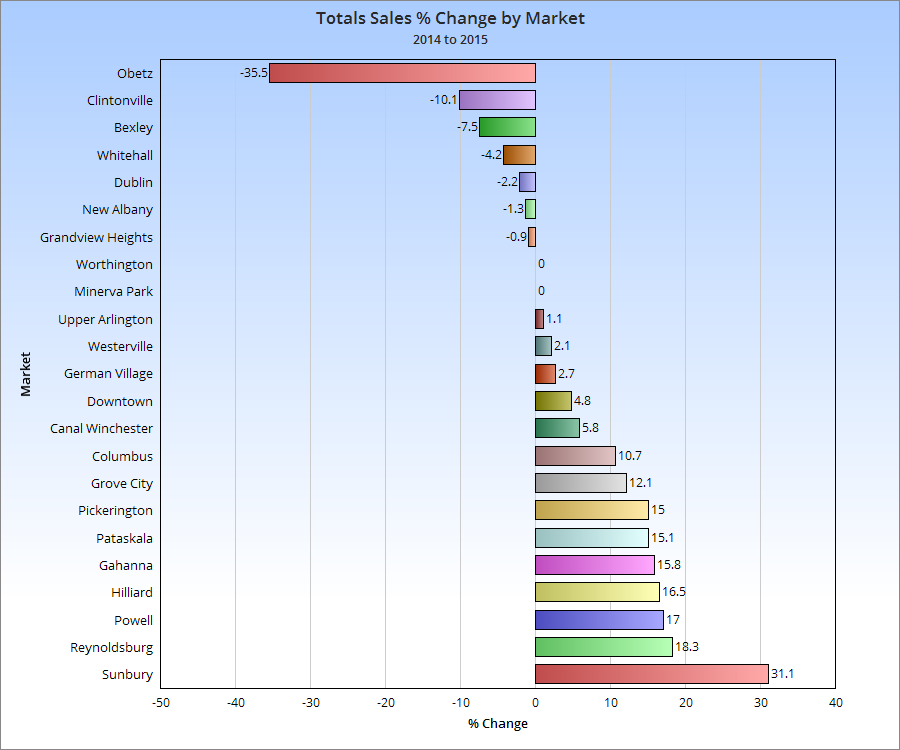

That lack of inventory really shows up in the yearly % change chart. Few urban markets have increased year over year, as they have a much more limited supply of housing, even as demand for urban housing has increased.

Let’s see how this impacted prices.

While urban markets were not necessarily the most expensive compared to suburban, more of them were generally towards the top half of price increases last year.