I posted a graph recently showing housing permits for Franklin County to show how construction was trending. Today, I found more long-term data for both the city and county that continue to show some interesting Columbus housing trends. All data comes from the Building Permits Survey.

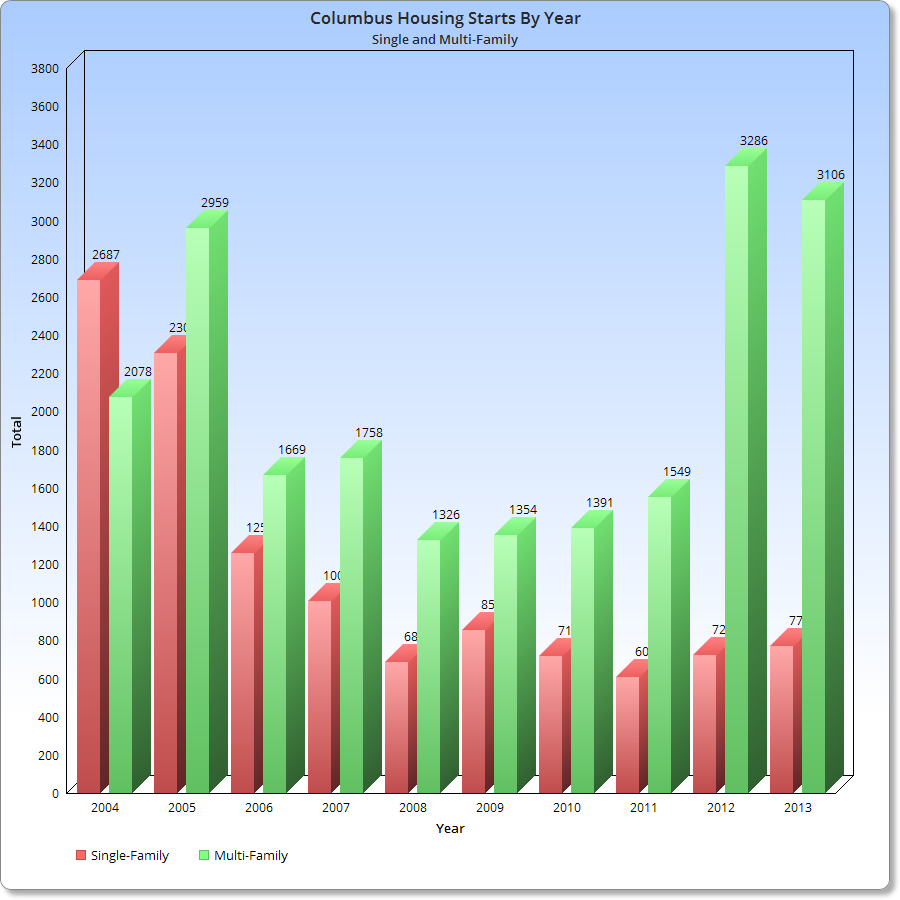

First, let’s look at just the city of Columbus.

The chart above goes back through the mid-1990s. The first thing to notice is the housing boom from 1999-2002. Both single-family and multi-family construction was booming. The very good economic conditions, or seemingly good ones, during the 1999-2000 period is probably most responsible for this. What’s most interesting is that the boom seemed to last through at least part of the mild recession experienced in 2001-2002. After that, housing of both types started to decline through the late 2000s. This shows that construction in the city began to decline as early as 2002-2003, before the peak of the general housing boom in the mid-2000s.

Another interesting fact is at the end of the period. Multi-family units have recovered and are back in boom territory. This boom, however, is much different than the one that occurred more than a decade ago, as shown by the below chart.

During the 1999-2002 housing boom, multi-family housing averaged 59.3% of all the units constructed. In the current boom, which began in 2012, multi-family housing has averaged 82.1% of all the units constructed. The average difference between the types 1999-2002 was just 18.6 points. In the current boom, the difference is an amazing 64.2 points! In that regard, there really is no comparison between the housing boom a decade ago and the current one. Multi-family construction is in MUCH higher relative demand now than it was at any time in the last 17-18 years, including during the last housing boom.

But what does this tell us about where the housing is actually being constructed? Well, for that, we have to look at the entirety of Franklin County. Is the county also seeing a similar multi-family boom, or has single-family construction recovered there more than in the city?

This chart, in some aspects, is the opposite of the one for the city. While in the city, multi-family units consistently outnumbered single-family, the opposite is true for the county as a whole. This is likely because the county takes into account all the suburban areas, most of which are dominated by single-family housing. In only a few instances did multi-family housing units outnumber single-family before 2010. After 2010, it’s clear that the multi-family boom is hitting the rest of the county and not just Columbus itself. This may actually represent an even greater shift in housing construction.

Here’s the % of total chart for the county.

So it’s also clear that the county is seeing most of its construction in recent years be multi-family units.

But this still doesn’t tell us if most of Franklin County’s housing construction is occurring in the city or in the suburbs. The easiest way to tell is to take the city totals and find out the % of total to the overall county.

Not much can be taken from this chart, however. Columbus encompasses the largest part of Franklin County by far, so it has always included most of the county’s construction. Perhaps a better way to look at it would be to measure the city’s total against the overall metro share, but that’s for another day.